Economics

2iec & 1iec

Overview of 2iec

- Basic economic ideas and resource allocation

- The price system and the microeconomy

- Government microeconomic intervention

- The macroeconomy

- Government macroeconomic intervention

- International economic issues

Overview of 1iec

- The price system and the microeconomy

- Government microeconomic intervention

- The macroeconomy

- Government macroeconomic intervention

- International economic issues

Structured Writing - Simple Model

Structured Writing - Intermediate Model

Structured Writing - Advanced Model

sample essays on ...

- monopoly

- labour supply

- protectionism

- globalisation

- interest rate

- development

monopoly

- Read: Tesla holds 80% of US EV market despite losing federal tax credit

- Evaluate whether a monopoly is likely to operate efficiently. Refer to at least one monopoly of your choice.

labour supply

- Read: The five UK sectors grappling with acute labour shortages

- Evaluate the factors that might influence the supply of labour in an occupation of your choice.

protectionism

- Read: IMF warns there is 'limited ammunition' to fight recession

- Evaluate the likely impact of an increase in protectionism on the global economy.

globalisation

- Read: The modern era of globalisation is in danger

- Evaluate the likely impact of globalisation on the global economy.

interest rates

- Evaluate the microeconomic and macroeconomic effects of decreasing interest rates in Kenya, or another developing country of your choice.

development

- Evaluate the microeconomic and macroeconomic strategies that could be used to promote development in Kenya, or another developing country of your choice.

Flipped classroom - Video ressources

List of videos on economic conceptsStudy plan (2iec)

Part 1: Basic economic ideas and resource allocation

- Scarcity, choice and opportunity cost

- Economic methodology

- Factors of production

- Resource allocation in different economic systems

- Production possibility curves

- Classification of goods and services

Chapter 1: Scarcity, choice and opportunity cost

- fundamental economic problem

- resources

- wants

- needs

- scarcity

- choice

- factors of production

- firm

- opportunity cost

Chapter 1: Scarcity, choice and opportunity cost

- wants

- needs

- resources

- economic problem

- opportunity cost

- scarcity and choice

fundamental economic problem

- scarce resources ...

- ... but unlimited wants.

resources

- inputs available ...

- ... for the production ...

- ... of goods and services

wants

- the goods and services ...

- ... that people may like to have ...

- ... but are not always realised

needs

- things that are necessary for survival ...

- ... such as food

scarcity

- a situation ...

- ... in which wants and needs ...

- ... are greater than ...

- ... the resources available

choice

- resources are scarce ...

- ... so individuals, firms and governments ...

- ... have to consider alternatives

factors of production

- resources or inputs ...

- ... available in an economy ...

- ... that are used in the production ...

- ... of goods and services

firm

- any business ...

- ... that hires factors of production ...

- ... to produce good and services

opportunity cost

- the cost expressed ...

- ... in terms of ...

- ... the next best alternative forgone ...

- ... when a choice is made

basic economic problem

Credit: "Pittsburgh Homeless" by "daveyinn"/Flickr Creative Commons, CC BY 2.0

choices and tradeoffs

Credit: modification of "College of DuPage Commencement 2018 107" by COD Newsroom/Flickr, CC BY 2.0

budget constraint

Each point on the budget constraint represents a combination of burgers and bus tickets whose total cost adds up to Alphonso's budget of $10. The relative price of burgers and bus tickets determines the slope of the budget constraint. All along the budget set, giving up one burger means gaining four bus tickets.

resources

- inputs available ...

- ... for the production of goods and services

opportunity cost

scarcity

- situation that arises because

- people have unlimited wants

- in the face of limited resources

scarcity and choice

- choices are made

- by different agents : households, firms, government, banks, ...

- at different levels : microeconomic level, macroeconomic level

Japan's population decline

- Suggest the likely effect of the changes in Japan's population on:

- what to produce

- how to produce

- for whom to produce

Chapter 2: Economic methodology

- positive statement

- normative statement

- value judgement

- ceteris paribus

- economic law

- microeconomics

- macroeconomics

- short run

- long run

- very long run

positive statement and normative statement

Economics seeks to describe economic behavior as it actually exists. Philosophers draw a distinction between positive statements, which describe the world as it is, and normative statements, which describe how the world should be.

Positive statements are factual. They may be true or false, but we can test them, at least in principle.

Normative statements are subjective questions of opinion.

value judgement

- a statement based on your opinion or belief, ...

- ... rather than on facts

ceteris paribus

- other things being equal

- analyse the changes in one variable ...

- ... while holding other influences constant

model

- a simplified view of reality ...

- used to explain economic problems and issues

microeconomics

- the study of individual markets

- households

- firms

microeconomics - consumer's behaviour

What determines how households and individuals spend their budgets?

What combination of goods and services will best fit their needs and wants, given the budget they have to spend?

How do people decide whether to work, and if so, whether to work full time or part time?

microeconomics - producer's behaviour

What determines the products, and how many of each, a firm will produce and sell?

What determines the prices a firm will charge?

What determines how a firm will produce its products?

What determines how many workers it will hire?

How will a firm finance its business?

macroeconomics

- the study of an economy or a group of economies

short run

- time period ...

- ... when a firm can change at least one ...

- ... but not all factor inputs

long run

- time period ...

- ... when all factors of production are variable ...

- ... but with a constant, ...

- ... such as the state of technology

very long run

- time period ...

- ... when all key inputs into production ...

- ... are variable

Chapter 3: Factors of production

- primary sector

- secondary sector

- tertiary sector

- land

- labour

- capital

- enterprise

- entrepreneur

- human capital

- physical capital

Chapter 3: Factors of production

- rent

- wage

- salary

- interest

- profit

- specialisation

- division of labour

- Adam Smith

- enterprise culture

circular flow diagram

circular flow diagram : model with 2 agents

factors of production

- land

- labour

- capital

- enterprise

entrepreneur

- individual ...

- ... who seeks out new business opportunities ...

- ... and is willing to take risks

land

- factor of production ...

- ... natural resources in an economy

labour

- factor of production

- human resources available in a country

capital

- factor of production

- physical resource ...

- ... made by humans ...

- ... that aids the production ...

- ... of goods and services

enterprise

- factor of production

- organising production, and ...

- ... taking risks

physical capital

- factor of production

- Examples

- machinery

- buildings

- infrastructure

human capital

- value of labour ...

- .. to the productive potential (future growth) of an economy

- Examples:

- education

- health

- skills

production

obtained by combining factors of production

$\text{Quantity Produced} = f( \text{land}, \text{labour}, \text{capital}, \text{enterprise} ) $

production depends on the quantity and quality of these factors of production

low-income economies

- economies where ...

- ... income per head ...

- ... was 1025 USD or less in 2018 (World Bank)

low middle-income economies

- economies where ...

- ... income per head ...

- ... was between 1026 USD and 3995 USD in 2018 (World Bank)

high income economies

- economies where ...

- ... income per head ...

- ... was 12.376 USD or more in 2018 (World Bank)

specialisation

the process by which ...

... individuals, firms and economies ...

... concentrate on producing those goods and services ...

... where they have an advantage over others

division of labour

- where a manufacturer process ...

- ... is split into a sequence of individual tasks

Credit: "Red Wing Shoe Factory Tour" by Nina Hale/Flickr Creative Commons, CC BY 2.0

Adam Smith

Credit: "Adam Smith" by Cadell and Davies (1811), John Horsburgh (1828), or R.C. Bell (1872)/Wikimedia Commons, Public Domain

Adam Smith

1. The Wealth of Nations by Adam Smith2. The Division of Labour

Adam Smith

Chapter 4: Resource allocation in different economic systems

- allocative mechanism

- market economy or market system

- market

- planned (or command) economy

- mixed economy

- transitional economy

- private sector

- public sector

- privatisation

- emerging economy

allocative mechanism

choices have to be made ...

... because of the problem of scarcity.

How choices are made ...

... depends on the economic system

3 main types of economic system

- market economy : decisions driven by market mechanism

- planned economy

- mixed economy

planned economy

Credit: "Pyramids at Giza" by Jay Bergesen/Flickr Creative Commons, CC BY 2.0

market economy

Credit: work by Erik Drost/Flickr Creative Commons, CC BY 2.0

index of economic freedom

price mechanism

excess supply of firms

$\longrightarrow$ fall in price

$\longrightarrow$ firms less willing to supply

$\longrightarrow$ increase in price

$\longrightarrow$ more firms now willing to supply

$\longrightarrow$ increase in supply

$\longrightarrow$ fall in price ...

market economy: role of the government

- role of watching that the price mechanism works efficiently

- market failure: if price mechanism does not work efficiently

market economy: role of the government

- role of watching that the price mechanism works efficiently

- market failure: if price mechanism does not work efficiently

- Examples of market failure:

- healthcare being underprovided by private sector

- private sector not providing fire services

- ...

planned economy: Commissariat général du Plan (1946-2006)

planned economy

- central government is responsible ...

- ... for the allocation of resources.

- Examples of controls:

- production targets are set

- prices and wages are controlled

mixed economy

- both private sector and public sector play a role

- decision is result of interaction between firms, labour and government

- private and public ownership coexist

- privatisation: trend over the past decades

private sector

- that part of an economy ...

- ... under private ownership

public sector

- that part of the economy ...

- ... under government ownership

privatisation

- where there is a change in ownership ...

- ... from the public ...

- ... to the private sector

emerging economy

- one that is making quick progress ...

- ... towards becoming a high-income economy

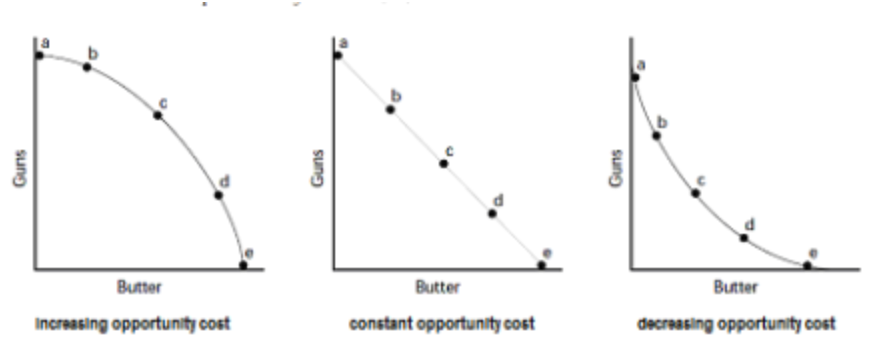

Chapter 5: Production possibility curves

- production possibility curve (or frontier)

- scarcity and choice

- economic growth

- trade-off

- productive capacity

learning objectives

- meaning and purpose of PPC

- shape of PPC: constant opportunity costs vs. increasing opportunity costs

- causes and consequences of a shift of PPC

resources and the PPC

- high-income economies: wide availability of factors of production

- low-income economies: few ressources and poor quality of resources

trade-off

- what is involved in deciding ...

- ... whether to give up one good ...

- ... for another good

productive capacity

- the maximum output ...

- ... that can be produced ...

- ... when all resources are used fully

A Healthcare vs. Education Production Possibilities Frontier

This production possibilities frontier shows a tradeoff between devoting social resources to healthcare and devoting them to education.

At A all resources go to healthcare and at B, most go to healthcare. At D most resources go to education, and at F, all go to education.

Productive and Allocative Efficiency

Production Possibility Frontier for the U.S. and Brazil

The Tradeoff Diagram

shape of PPC

- constant opportunity cost:

- increasing opportunity cost:

tutorial video 1

production possibilities curve as a model of a country's economy

tutorial video 2

PPCs for increasing, decreasing and constant opportunity cost

tutorial video 3

opportunity cost and comparative advantage using a PPC and an output table

Chapter 6: Classification of goods and services

- free good

- private good

- rivalry

- excludability

- public good

- non-excludability

- non-rivalry

- free rider

Chapter 6: Classification of goods and services

- government expenditure

- non-rejectability

- merit good

- information failure

- market imperfection

- market failure

- demerit good

learning objectives

- meaning of:

- free goods and private goods

- public goods

- merit goods and demerit goods

- imperfect information in the market

excludability

- a good is excludable ...

- ... if other consumers can be prevented ...

- ... from using or consuming it.

rivalry

- a good is rival ...

- ... if only one person can consume it ...

- ... and therefore the good is not available for other consumers

non-rival good

- a good is non-rival ...

- ... when the amount available to others ...

- ... does not diminish.

determining the type of good

| excludable | non-excludable | |

|---|---|---|

| rival | private good | quasi-public good |

| non-rival | quasi-public good | public good |

private good

- private goods are bought and consumed ...

- ... by individual consumers or firms ...

- ... for their own benefit.

- private goods have two characteristics:

- excludability (i.e. by charging a price)

- rivalry (reduces availability)

free good

- goods that have zero opportunity cost ...

- ... since consumption is not limited by scarcity.

public good

- goods that have two characteristics ...

- non-excludable

- non-rival

quasi-public good

- goods that have two characteristics ...

- excludable

- non-rival

merit goods

- a good that is thought to be desirable ...

- ... but which is underprovided by the market.

demerit goods

- a good that is thought to be undesirable ...

- ... but which is overprovided by the market.

Positive externalities and public goods

Introduction to public good (Voyager and NASA)Part 2: The price system and the microeconomy

- Demand and supply curves

- Price elasticity, income elasticity and cross elasticity of demand

- Price elasticity of supply

- The interaction of demand and supply

- Consumer and producer surplus

Chapter 7: Demand and supply curves

- price mechanism

- consumers

- market

- demand

- supply

- supply chain

- notional demand

- effective demand

- demand curve (D)

- market demand

Chapter 7: Demand and supply curves

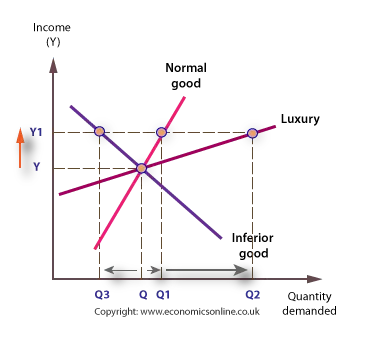

- demand schedule

- movement along a demand curve

- normal goods

- inferior goods

- substitute

- complement

- joint demand

- supply curve (S)

- supply schedule

- subsidies

Chapter 7: Demand and supply curves

- indirect tax

- extension of demand or supply

- contraction of demand or supply

Chapter 7: Demand and supply curves

- effective demand

- demand

- law of demand

- demand curve

- demand schedule

- derived demand

- supply curve

- supply schedule

- change in quantity demanded

- extension in demand

Chapter 7: Demand and supply curves

- contraction in demand

- change in quantity supplied

- extension in supply

- contraction in supply

- change in demand

- composite demand

- normal good

- inferior good

- indirect taxes

- subsidy

price mechanism

- the means of allocating resources ...

- ... in a market economy

consumers

- individuals or households ...

- ... who buy goods and services ...

- ... for their own use or for others

market

- where buyers and sellers ...

- ... get together to trade

demand

- the quantity of a product ...

- ... that consumers are willing and able ...

- ... to buy at different prices ...

- ... per period of time ...

- ... other things equal, ceteris paribus

supply

- the quantity of a product ...

- ... that producers are willing and able ...

- ... to sell at different prices ...

- ... within a time period ...

- ... other things equal, ceteris paribus

supply chain

- all the stages of a product's progress ...

- ... from raw materials, production ...

- ... and distributions ...

- ... until it reaches the consumer

notional demand

- where buyers may want to buy a product ...

- ... but which is not always backed up ...

- ... by the ability to pay

effective demand

- demand that is supported ...

- ... the ability to pay

demand curve (D)

- a line plotted on a graph ...

- ... that represents the relationship between ...

- ... the quantity demanded ...

- ... and the price of a product

market demand

- the total amount demanded ...

- ... by consumers

demand schedule

- the data from which ...

- ... a demand curve is drawn on a graph

movement along a demand curve

- shows how quantity demanded ...

- ... responds to a change in price

normal goods

- where the quantity demanded ...

- ... increases as income increases

inferior goods

- where the quantity demanded ...

- ... increases as income decreases

substitute

- an alternative good

complement

- a good consumed with another

joint demand

- when two goods ...

- ... are consumed together

supply curve (S)

- a line plotted on a graph ...

- ... that represents the relationship ...

- ... between the quantity supplied ...

- ... and the price of the product

supply schedule

- the data from which ...

- ... a supply curve is drawn on a graph

subsidies

- direct payments ...

- ... made by governments ...

- ... to producers of goods and services

indirect tax

- a tax levied ...

- ... on goods and services ...

- ... such as a general sales tax

extension of demand or supply

- an increase in the ...

- ... quantity demanded ...

- ... or quantity supplied

contraction of demand or supply

- a decrease in the ...

- ... quantity demanded ...

- ... or quantity supplied

price mechanism

- the means of allocating resources ...

- ... in a market economy

consumers

- individuals or households ...

- ... who buy goods and services ...

- ... for their own use or for others

market

- where buyers and sellers ...

- ... get together to trade

demand

- the quantity of a product ...

- ... that consumers are willing and able to buy ...

- ... at different prices per period of time ...

- ... other things equal, ceteris paribus

supply

- the quantity of a product ...

- ... that producers are willing and able to sell ...

- ... at different prices per period of time ...

- ... other things equal, ceteris paribus

supply chain

- all the stages of product's progress ...

- ... from raw materials, production and distribution ...

- ... until it reaches the consumer

notional demand

- where buyers may want to buy a product ...

- ... but which is not always backed up by the ability to pay

effective demand

- demand that is supported by the ability to pay

demand curve (D)

- a line plotted on a graph ...

- ... that represents the relationship between ...

- ... the quantity demanded and the price of a product

market demand

- total amount demanded by consumers

demand schedule

- data from which a demand curve is drawn on a graph

normal goods

- where the quantity demanded increases ...

- ... as income increases

inferior goods

- where the quantity demanded increases ...

- ... as income decreases

normal and inferior goods

inferior goods

substitute goods

- an alternative good

complement goods

- a good consumed with another

supply curve (S)

- a line plotted on a graph ...

- ... that represents the relationship between ...

- ... the quantity supplied and the price of the product.

supply schedule

- the data from which ...

- ... a supply curve is drawn on a graph

subsidies

- direct payments made by governments ...

- ... to producres of goods and services

indirect tax

- a tax levied on goods and services, ...

- ... such as a general sales tax

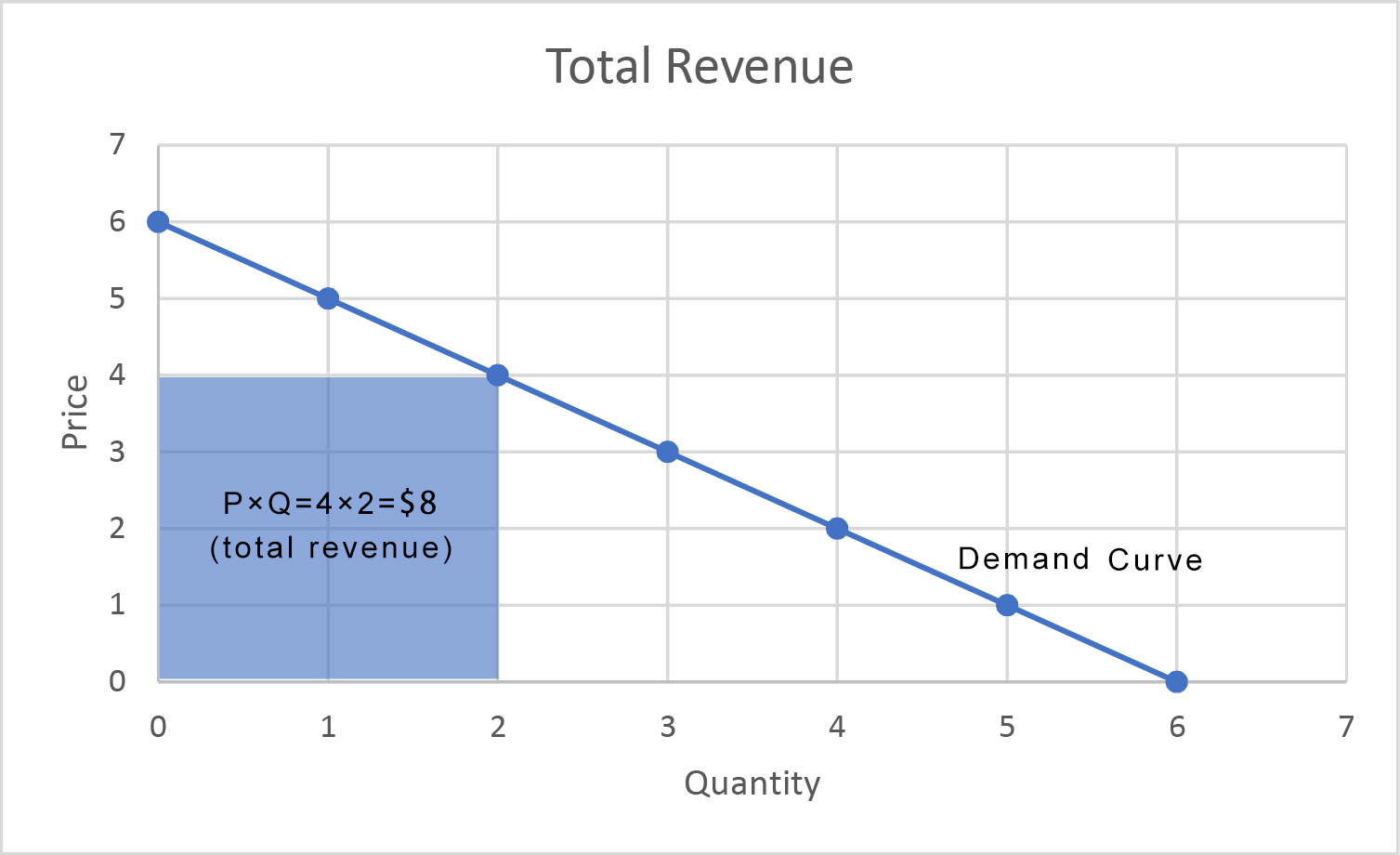

A Choice between Consumption Goods

How a Change in Income Affects Consumption Choices

How a Change in Price Affects Consumption Choices

The Foundations of a Demand Curve

|

|

An Example of Housing (a) As the price increases from P0 to P1 to P2 to P3, the budget constraint on the upper part of the diagram rotates clockwise. The utility-maximizing choice changes from M0 to M1 to M2 to M3. As a result, the quantity demanded of housing shifts from Q0 to Q1 to Q2 to Q3, ceteris paribus. (b) The demand curve graphs each combination of the price of housing and the quantity of housing demanded, ceteris paribus. The quantities of housing are the same at the points on both (a) and (b). Thus, the original price of housing (P0) and the original quantity of housing (Q0) appear on the demand curve as point E0. The higher price of housing (P1) and the corresponding lower quantity demanded of housing (Q1) appear on the demand curve as point E1. |

Farmer’s Market

Credit: modification of "Old Farmers' Market" by NatalieMaynor/Flickr, CC BY 2.0

Weirdest Celebrity Items Sold At Auction

Britney Spears' Gum, Brad Pitt's Breath And More (Huffpost)A Demand Curve for Gasoline

A Supply Curve for Gasoline

Shifts in Demand: A Car Example

Demand Curve

Demand Curve with Income Increase

Demand Curve Shifted Right

Factors That Shift Demand Curves

(b) The same factors, if their direction is reversed, can cause a decrease in demand from D0 to D1.

Shifts in Supply

Supply Curve

Setting Prices

Increasing Costs Leads to Increasing Price

Supply Curve Shifts

Factors That Shift Supply Curves

(b) The same factors, if their direction is reversed, can cause a decrease in supply from S0 to S1.

videos and tutorial

supply, demand and market equilibrium(Khan Academy)

law of demand

market demand as the sum of individual demand

supply, demand and market equilibrium

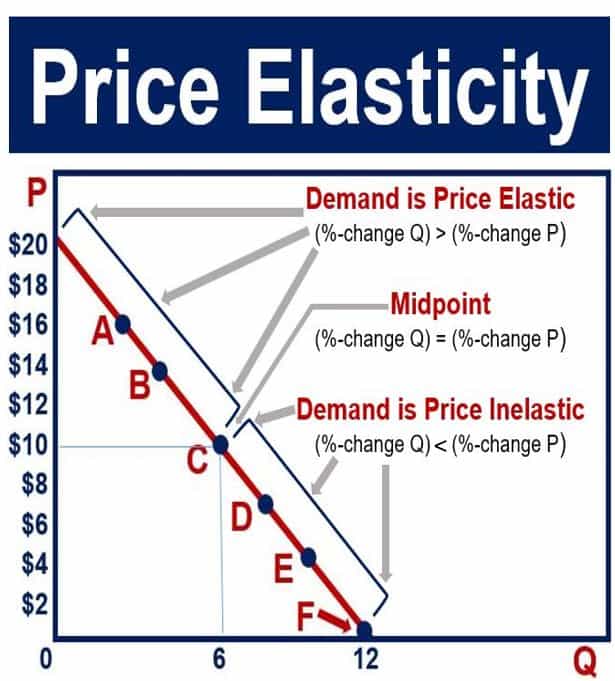

Chapter 8: Price elasticity, income elasticity and cross elasticity of demand

- elasticity

- elastic

- inelastic

- price elasticity of demand (PED)

- price elastic

- price inelastic

- perfectly inelastic

- perfectly elastic

Chapter 8: Price elasticity, income elasticity and cross elasticity of demand

- unit elasticity

- income elasticity of demand (YED)

- necessity good

- superior good

- cross elasticity of demand (XED)

Chapter 8: Price elasticity, income elasticity and cross elasticity of demand

- price elasticity of demand

- income elasticity of demand

- cross elasticity of demand (or cross-price elasticity of demand)

- substitute goods

- complementary goods

- perfectly inelastic

Chapter 8: Price elasticity, income elasticity and cross elasticity of demand

- inelastic

- unitary elasticity

- elastic

- perfectly elastic

- total revenue

elasticity

- a numerical measure of responsiveness ...

- ... of one variable following ...

- ... a change in another variable ...

- ceteris paribus or other things equal

elastic

- where the relative change ...

- ... in the quantity demanded ...

- ... is greater than ...

- ... the change in price, income ...

- ... or the prices of substitutes ...

- ... and complements

inelastic

- where the relative change ...

- ... in the quantity demanded ...

- ... is less than ...

- ... the change in price, income ...

- ... or the prices of substitutes ...

- ... and complements

price elasticity of demand (PED)

- measures of the responsiveness ...

- ... of the quantity demanded ...

- ... for a product following ...

- ... a change in the price of the product

price elastic

- when the relative change ...

- ... in the quantity demanded ...

- ... is greater than ...

- ... the change in price of the product

price inelastic

- when the relative change ...

- ... in the quantity demanded ...

- ... is less than ...

- ... the change in price of the product

perfectly inelastic

- where a change in price ...

- ... has no effect on the quantity demanded

perfectly elastic

- where all that is produced ...

- ... is sold at a given price

unit elasticity

- where the change in price ...

- ... is relatively the same as ...

- ... the change in quantity demanded

income elasticity of demand (YED)

- measures the responsiveness ...

- ... of the quantity demanded ...

- ... for a product following ...

- ... a change in income

necessity good

- a type of normal good ...

- ... with a YED ...

- ... that is close to zero

superior good

- a good with ...

- ... a YED ...

- ... greater than 1

cross elasticity of demand (XED)

- measures the responsiveness ...

- ... of the quantity demanded ...

- ... for one product ...

- ... following a ...

- ... change in the price ...

- ... of another product

On-Demand Media Pricing

Credit: modification of “160906_FF_CreditCardAgreements” by kdiwavvou/Flickr, Public Domain

elasticity

- a numerical measure of responsiveness ...

- ... of one variable following a change in another variable ...

- ... ceteris paribus

elastic

- where the relative change ...

- ... in the quantity demanded is greater ...

- ... than the change in price, income ...

- ... or the prices of substitutes and complements .

inelastic

- where the relative change ...

- ... in the quantity demanded is less ...

- ... than the change in price, income ...

- ... or the prices of substitutes and complements .

price elasticity of demand (PED)

- measures of the responsiveness ...

- ... of the quantity demanded for a product ...

- ... following a change in the price of the product.

$PED = \frac{ \text{% change in quantity demanded} }{ \text{% change in price} }$

price elastic

- when the relative change in the quantity demanded ...

- ... is greater than ...

- ... change in price of the product.

price inelastic

- when the relative change in the quantity demanded ...

- ... is less than ...

- ... change in price of the product.

perfectly inelastic

- where a change in price ...

- ... has no effect ...

- ... on the quantity demanded

perfectly elastic

- where all that is produced ...

- ... is sold at ...

- ... a given price

unit elasticity

- where the change in price is ...

- ... relatively the same as ...

- ... the change in quantity demanded

price elasticity explained using a diagram

income elasticity of demand (YED)

- measures the responsiveness ...

- ... of the quantity demanded for a product ...

- ... following a change in income.

necessity good

- a type of normal good with a YED ...

- ... that is close to zero

superior good

- a good with a YED greater than 1

relationships between a change in income and quantity demanded

cross elasticity of demand (XED)

- measures the responsiveness of the ...

- ... quantity demanded ...

- ... for one product following ...

- ... a change in the price of another product.

$XED = \frac{ \text{% change in quantity demanded of product A} }{ \text{% change in the price of product B} }$

Calculating the Price Elasticity of Demand

Four part question (1/3)

- Define price elasticity of demand and explain how it is calculated. Provide two hypothetical examples of luxury goods, one with elastic demand and one with inelastic demand. Justify your classification for each example.

- Suppose the government imposes a significant tax increase on luxury cars to generate revenue. Analyze how this tax increase is likely to affect the price, quantity demanded, and total revenue in the luxury car market. Support your analysis with the appropriate elasticity concept.

Four part question (2/3)

- Calculate income elasticity for luxury cars if, over a year, the average income in the country increased by 10%, and the quantity demanded of luxury cars increased by 15%.

- Additionally, calculate the cross elasticity of demand between luxury cars and economy cars if the price of economy cars increased by 8%, and the quantity demanded of luxury cars decreased by 12%.

Four part question (3/3)

- Discuss the implications of the calculated income and cross elasticities for luxury car manufacturers. What do these elasticities reveal about the nature of luxury cars as normal or inferior goods and their relationship with economy cars?

- Provide recommendations for luxury car manufacturers based on your analysis.

Chapter 9: Price elasticity of supply

- price elasticity of supply

- price elastic supply

- price inelastic supply

- stocks

- perishability

price elasticity of supply (PES)

- a numerical measure ...

- ... of the responsiveness of the quantity supplied ...

- ... to a change in the price of the product

$PES = \frac{ \text{% change in quantity supplied} }{ \text{% change in price} }$

price elastic supply

- the quantity supplied ...

- ... responds more than proportionately ...

- ... to a change in its price

price inelastic supply

- the quantity supplied ...

- ... responds less than proportionately ...

- ... to a change in its price

factors affecting price elasticity supply

- number of producers

- amount of stocks

- time period

- existence of spare capacity

- length of the production period

- degree of factor mobility

Price Elasticity of Supply

Infinite Elasticity

Zero Elasticity

A Constant Unitary Elasticity Demand Curve

A Constant Unitary Elasticity Supply Curve

Passing along Cost Savings to Consumers

Passing along Higher Costs to Consumers

Elasticity and Tax Incidence

Elasticity and Tax Incidence

How a Shift in Supply Can Affect Price or Quantity

How a Shift in Supply Can Affect Price or Quantity

Chapter 10: The interaction of demand and supply

- equilibrium

- disequilibrium

- equilibrium price

- equilibrium quantity

- joint demand

- alternative demand

- derived demand

Chapter 10: The interaction of demand and supply

- joint supply

- rationing

- signalling

- price mechanism

- transmission of preferences

- incentivisation

- scarcity and choice

Demand and Supply Curves

Fall in supply

Good Weather for Salmon Fishing: The Four-Step Process

The Print News Market: A Four-Step Analysis

Higher Compensation for Postal Workers

Combined Effect of Decreased Demand and Decreased Supply

Shifts of Demand or Supply versus Movements along a Demand or Supply Curve

Demand and Supply Curves

Demand and Supply Curves

The figure displays a generic demand and supply curve.

Demand and Supply Curves

The horizontal axis shows the different measures of quantity: a quantity of a good or service, a quantity of labor for a given job, or a quantity of financial capital.

Demand and Supply Curves

The vertical axis shows a measure of price: the price of a good or service, the wage in the labor market, or the rate of return (like the interest rate) in the financial market.

Demand and Supply Curves

We can use the demand and supply curves to explain how economic events will cause changes in prices, wages, and rates of return.

Impact of Increasing Demand for Nurses 2020–2030

In 2020, the median salary for nurses was 75,330 USD. As demand for services increases, the demand curve shifts to the right (from $D_0$ to $D_1$) and the equilibrium quantity of nurses increases from $Qe_0$ to $Qe_1$. The equilibrium salary increases from $Pe_0$ to $Pe_1$.

Impact of Decreasing Supply of Nurses between 2020 and 2030

The increase in demand for nurses shown in the figure leads to both higher prices and higher quantities demanded. As nurses retire from the work force, the supply of nurses decreases, causing a leftward shift in the supply curve and higher salaries for nurses at $Pe_2$. The net effect on the equilibrium quantity of nurses is uncertain, which in this representation is less than $Qe_1$, but more than the initial $Qe_0$.

The effect of a 30% salt tax

The initial equilibrium. Initially the market equilibrium is at point A. The price is $P^*$ and the quantity of salt sold is $Q^*$.

The effect of a 30% salt tax

A 30% tax. A 30% tax is imposed on suppliers. Their marginal costs are effectively 30% higher at each quantity. The supply curve shifts.

The effect of a 30% salt tax

The new equilibrium. The new equilibrium is at B. The price paid by consumers has risen to $P_1$ and the quantity has fallen to $Q_1$.

The effect of a 30% salt tax

The tax paid to the government. The price received by suppliers (after they have paid the tax) is $P_0$. The double-headed arrow shows the tax paid to the government on each unit of salt sold.

Chapter 11: Consumer and producer surplus

- consumer surplus

- producer surplus

consumer surplus

- the difference between ...

- ... the price ...

- ... a consumer is willing to pay for a product ...

- ... and its market price

producer surplus

- the difference between ...

- ... the price ...

- ... a producer is willing to accept ...

- ... and what is actually paid

Demand and Supply for Gasoline

Demand and Supply for Gasoline

The demand curve (D) and the supply curve (S) intersect at the equilibrium point E, with a price of 1.40 dollar and a quantity of 600. The equilibrium price is the only price where quantity demanded is equal to quantity supplied. At a price above equilibrium like 1.80 dollar, quantity supplied exceeds the quantity demanded, so there is excess supply. At a price below equilibrium such as 1.20 dollar, quantity demanded exceeds quantity supplied, so there is excess demand.

Consumer and Producer Surplus

Consumer and Producer Surplus

The somewhat triangular area labeled by F shows the area of consumer surplus, which shows that the equilibrium price in the market was less than what many of the consumers were willing to pay. Point J on the demand curve shows that, even at the price of 90 dollar, consumers would have been willing to purchase a quantity of 20 million. The somewhat triangular area labeled by G shows the area of producer surplus, which shows that the equilibrium price received in the market was more than what many of the producers were willing to accept for their products. For example, point K on the supply curve shows that at a price of 45 dollar, firms would have been willing to supply a quantity of 14 million.

Efficiency and Price Floors and Ceilings

Efficiency and Price Floors and Ceilings

(a) The original equilibrium price is 600 dollar with a quantity of 20,000. Consumer surplus is T + U, and producer surplus is V + W + X. A price ceiling is imposed at 400 dollar, so firms in the market now produce only a quantity of 15,000. As a result, the new consumer surplus is T + V, while the new producer surplus is X. (b) The original equilibrium is $8 at a quantity of 1,800. Consumer surplus is G + H + J, and producer surplus is I + K. A price floor is imposed at 12 dollar, which means that quantity demanded falls to 1,400. As a result, the new consumer surplus is G, and the new producer surplus is H + I.

The effect of a 30% salt tax

- Identify the consumer surplus and producer surplus

- before the introduction of the tax

- after the introduction of the tax

- Discuss how taxes affect both surpluses.

consumer surplus and producer surplus

Part 3: Government microeconomic intervention

- Reasons for government intervention in markets

- Methods and effects of government intervention in markets

- Addressing income and wealth inequality

Chapter 12: Reasons for government intervention in markets

- market failure

- how governments intervene in markets

- controlling prices in markets

Chapter 13: Methods and effects of government intervention in markets

- impact & incidence of specific indirect taxes

- impact & incidence of subsidies

- direct provision of goods & services

- maximum & minimum prices

- buffer stock schemes

- provision of information

Chapter 14: Addressing income and wealth inequality

- income and wealth

- measuring income and wealth inequality

- economic reasons for inequality of income and wealth

- policies to redistribute income and wealth

Chapter 12: Reasons for government intervention in markets

- market failure

market failure

- when the free market ...

- ... does not make the best use ...

- ... of scarce resources

how do governments intervene in markets

- non-provision of public goods

- free rider problem

- private sector lack of interest

- opportunity cost of funding public goods

- over consumption of demerit goods

- under consumption of merit goods

controlling prices in markets

- set maximum prices

- use rent controls

- set minimum prices for agricultural products

controlling prices in markets - maximum prices

controlling prices in markets - maximum prices

controlling prices in markets - minimum prices

A Price Ceiling Example—Rent Control

European Wheat Prices: A Price Floor Example

Chapter 13: Methods and effects of government intervention in markets

- incidence

- maximum price

- minimum price

- buffer stock scheme

Chapter 13: Methods and effects of government intervention in markets

- indirect tax

- excise duty

- impact of tax

- incidence of tax

- specific tax

- subsidy

- impact of a subsidy

Chapter 13: Methods and effects of government intervention in markets

- incidence of a subsidy

- direct provision of goods and services

- maximum price

- minimum price

- price stabilisation

- buffer stock

incidence

- the extent to which ...

- ... the tax burden is borne ...

- ... by the producer ...

- ... or the consumer or both

maximum price (or price ceiling)

- a price that is fixed.

- the market price ...

- ... must not exceed this price.

minimum price (price floor)

- a price that is fixed.

- the market price ...

- ... must not go below this price.

buffer stock scheme

- a type of commodity agreement ...

- ... designed to limit price fluctuations

types of indirect taxes

- ad valorem : proportion or percentage of the price

- specific taxes : fixed amount per unit purchased

impact of indirect tax

- goal : discourage production and consumption of demerit goods

- tax imposed on the producer ...

- ... but passed on to consumers

impact of taxation

impact of taxation

impact of taxation

impact of taxation

impact of taxation

incidence of an indirect tax

- extent to which the tax burden is ...

- ... borne by the producer, ...

- ... by the consumer ...

- ... or by both

incidence of an indirect tax depends on ...

... the price elasticity of demand for the product

- the more inelastic the PED

$\longrightarrow$ easier it is to pass tax to the consumer

$\longrightarrow$ essential products are highly taxed - the more elastic the PED

$\longrightarrow$ consumer buys less as price $\uparrow$

$\longrightarrow$ producer will absorb tax

impact and incidence of subsidies

- ...

- ...

Chapter 14: Addressing income and wealth inequality

- wealth

- Gini coefficient

- informal economy

- minimum wage

- transfer payment

- progressive tax

- inheritance tax

- capital tax

Chapter 14: Addressing income and wealth inequality

- income

- wealth

- Gini coefficient

- minimum wage

- transfer payment

wealth

- a stock of assets ...

- ... that has been built up over time

Gini coefficient

- a numerical measure ...

- of income inequality

informal economy

- the part of the economy ...

- ... that is not regulated, protected or taxed ...

- ... by the government

minimum wage (expressed as wage per hour)

- the least amount ...

- ... an employer can ...

- ... legally pay one of its workers

transfer payment

- a payment made by ...

- ... the government ...

- ... to certain members of the community ...

- ... who may be unable to work ...

- ... or are in need of assistance

progressive tax

- one where the rate of taxation ...

- ... rises more than proportionately ...

- ... to the rise in income

inheritance tax

- a progressive tax ...

- ... on an inheritance or gift

capital tax

- a progressive tax paid ...

- ... annually ...

- ... on the difference between ...

- ... the buying and the selling price ...

- ... of an asset

difference between income and wealth

- income : reward for the services of a factor of production

- wages, salaries, bonuses

- rent, interest, profits

- wealth : stock of assets that someone has built up over time

- businesses, property

- shares, gold

- flow vs. stock

income $\longrightarrow$ flow concept

wealth $\longrightarrow$ stock concept

measuring income and wealth inequality

- Gini coefficient

- value $\longrightarrow$ 0 : equally distributed

- value $\longrightarrow$ 1 : inequality

economic reasons

for inequality of income & wealth

- no formal employment opportunities

- poor vocational training

- no investment in education & health sector

- poor infrastructure

- low rate of savings

- no access to loans

policies to redistribute income and wealth

- reduce income inequality

- redistribute wealth

$\longrightarrow$ dependent on tax revenues

policies to redistribute income and wealth

- minimum wage rates

- transfer payments

- taxation

- state provision of goods & services

minimum wage

- advantages

- reduces poverty

- disadvantages

- workers in informal sector are excluded

- self-employed workers are excluded

- critics say that it may create unemployment

- European countries by minimum wage

wage determination - minimum wage

transfer payment

- payment from tax revenue to vulnerable individuals

- examples

- pensions

- unemployment benefits

- housing allowances

- food coupons

- child benefits

- advantages vs. disadvantages

progressive tax

- high earners tax rate : 80%

- low earners tax rate : 20%-40%

- see real values for Luxembourg

$\longrightarrow$ reduces income differential

Part 4: The macroeconomy

- National income statistics

- Introduction to the circular flow of income

- Aggregate demand and aggregate supply analysis

- Economic growth

- Unemployment

- Price stability

Chapter 15: National income statistics

- national income

- gross domestic product (GDP)

- gross national income (GNI)

- net national income (NNI)

- at current market prices

- at constant prices

Chapter 15: National income statistics

- GDP deflator

- exports

- imports

- depreciation (of capital)

- net domestic product (NDP)

- net national product (NNP)

What is gross domestic product?

national income

- a country's total output

explore the national accounts data for Luxembourg (Statec)

national income statistics

- measures of the total output ...

- ... (income and expenditure) ...

- ... of an economy

gross domestic product (GDP)

- the total output ...

- ... produced in a country

gross domestic product (GDP)

Nominal gross domestic product (GDP) from OECD Real gross domestic product (GDP) from OECDgross national income (GNI)

- GDP ...

- ... plus net income ...

- ... from abroad

gross national income (GNI)

GNI data and definition (OECD)net property income from abroad

- receipts ...

- ... of profit, rent and interest ...

- ... earned on the ownership ...

- ... of foreign assets minus the payments ..

- ... of profit, rent and interest

- ... to non-residents

compensation of employees

- income of workers ...

- ... who work in another country ...

- ... for a short period of time

gross national disposable income

- GNI ...

- ... plus net transfers of workers' income ...

- ... to their relatives ...

- ... to and from other countries

multinational companies (MNCs)

- firms that operate ...

- ... in more than one country

circular flow of income

- a simplified view of ...

- ... how income flows ...

- ... around the economy

methods of measuring GDP

- output method

- income method

- expenditure method

output method

- a way of measuring GDP ...

- ... by calculating the total production ...

- ... of goods and services ...

- ... used in their production

value added

- the difference between ...

- ... the price at which products are sold ...

- ... and the price of goods and services ...

- ... used in their production

income method

- a way of measuring GDP ...

- ... by totalling all the incomes earned ...

- ... in producing the country's output

expenditure method

- a way of calculating GDP ...

- ... by totalling all the spending ...

- ... on the country's output

market prices

- prices paid ...

- ... by consumers ...

- ... that take into account ...

- ... indirect taxes and subsidies

basic prices

- prices charged by producers ...

- ... before the addition of indirect taxes ...

- ... and the deduction of subsidies

gross investment

- total spending on capital goods

net domestic product (NDP)

- GDP minus depreciation

net national income (NNI)

- gross national income (GNI) minus depreciation

net investment

- additions to the capital stock

depreciation (of capital goods)

- the value of capital goods ...

- ... that have worn out or become out-of-date

Chapter 16: Introduction to the circular flow of income

- circular flow of income

- closed economy

- open economy

- injection

- leakage (or withdrawal)

equilibrium income

Equilibrium point is where the savings line intersects with the investment line.

injection and leakage (or withdrawal)

Equilibrium income in a four-sector economy.

injection and leakage (or withdrawal)

At Y$_1$, we have leakages $>$ injections. Spending in the economy will decrease and therefore income will fall restoring the initial equilibrium.

injection and leakage (or withdrawal)

At Y$_2$, we have injections $>$ leakages. Spending in the economy will increase and therefore income will start rising restoring the initial equilibrium.

equilibrium income

The equality total investment $=$ total savings is essential for macroeconomic stability.

disequilibrium income

If savings exceed investment, it may indicate an excess of available funds, ... .

disequilibrium income

... which could lead to a decrease in interest rates or increased investment in the economy.

disequilibrium income

Excess saving and limited investment opportunities. There is an excess supply of funds in the financial markets ...

disequilibrium income

... borrowers are in a favourable position because lenders are competing to lend out their savings ...

disequilibrium income

... therefore lenders may be willing to accept lower interest rates.

disequilibrium income

In the context of lower interest rates, ...

disequilibrium income

... it becomes more attractive for borrowers to take out loans for investment projects.

Chapter 17: Aggregate demand and aggregate supply analysis

- aggregate demand (AD)

- aggregate supply (AS)

aggregate demand (AD)

- the total demand ...

- ... for an economy's goods and services ...

- ... at a given price level ...

- ... in a given time period

aggregate demand (AD)

$ \text{AD} = \text{C} + \text{I} + \text{G} + (\text{X}-\text{M}) $- $\text{C}$ : consumer expenditure

- $\text{I}$ : investment

- $\text{G}$ : government spending

- $\text{X}$ : exports of goods and services

- $\text{M}$ : imports of goods and services

consumer expenditure

- spending by households ...

- ... on goods and services

net exports

- exports minus imports

- $\text{NX} = \text{X} - \text{M}$

exchange rate

- the price ...

- ... of one currency ...

- ... in terms of ...

- ... another currency

aggregate supply (AS)

- the total output (real GDP) ...

- ... that producers in an economy ...

- ... are willing and able ...

- ... to supply ...

- ... at a given price level ...

- ... in a given time period

short-run aggregate supply (SRAS)

- the total output of an economy ...

- ... that will be supplied ...

- ... when there has not been enough time ...

- ... for the prices of factors of production ...

- ... to change

long-run aggregate supply (LRAS)

- the total output of a country ...

- ... supplied in the period ...

- ... when prices of factors of production ...

- ... have fully adjusted

average cost

- the cost ...

- ... per unit of output

supply-side shocks

- large and unexpected changes ...

- ... in short-run aggregate supply

Keynesians

- people who agree with the view of ...

- ... the economist John Maynard Keynes ...

- ... that government intervention ...

- ... is needed to achieve full employment

John Maynard Keynes (1883-1946)

new classical economist

- economists who think that ...

- ... the LRAS curve is vertical ...

- ... and that the economy will move towards ...

- ... full employment ...

- ... without government intervention

Keynesian Economics vs. Classic Economics

- Keynesian Economics

- increase consumer demand through government spending on:

- infrastructure

- unemployment benefits

- education

- government spending is necessary to maintain full employment

- Classic Economics

- promotes laissez-faire

- limit government intervention

- target firms not consumers

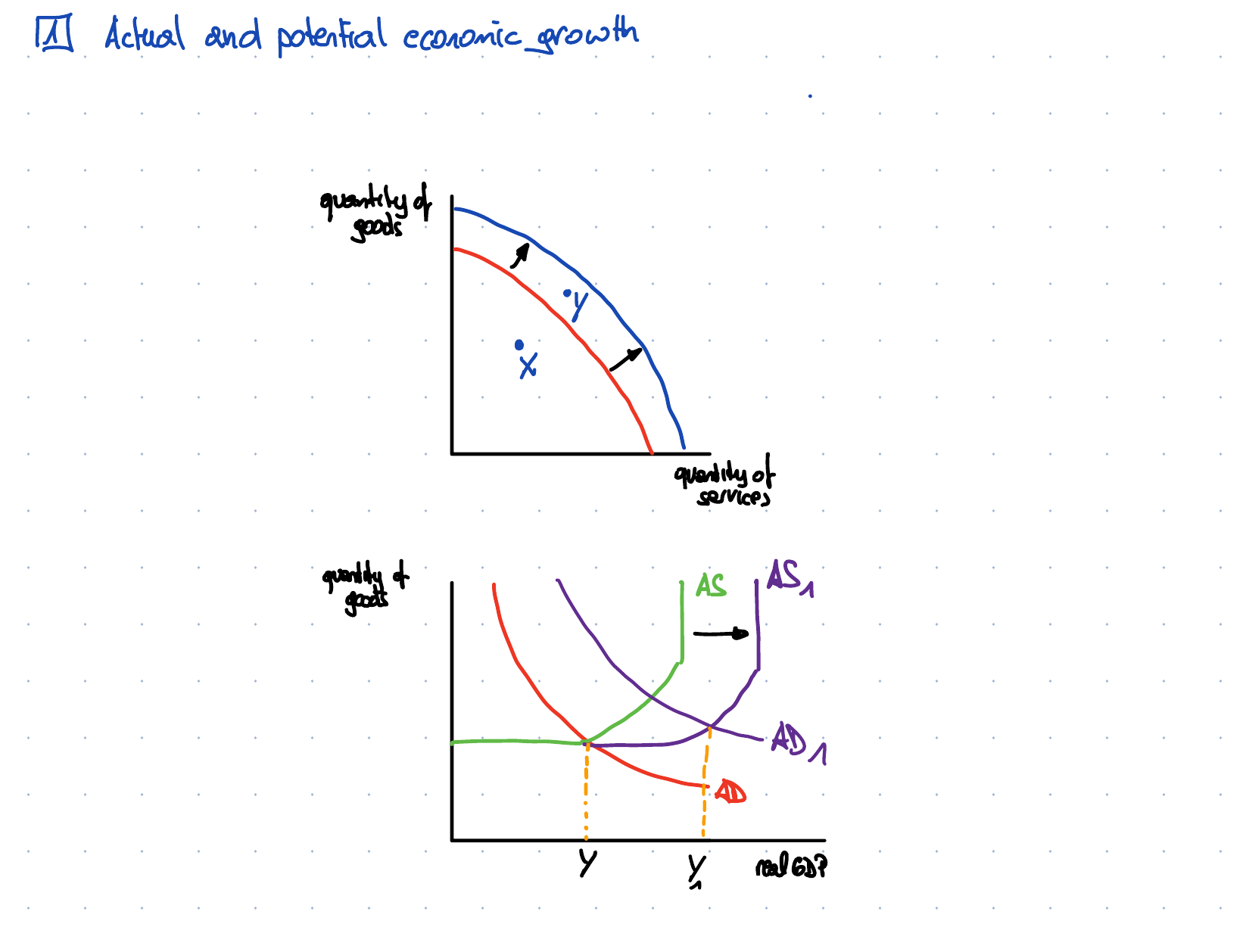

macroeconomic equilibrium

- the output and price level ...

- ... achieved where ...

- ... AD equals AS

aggregate demand and supply

Macroeconomic equilibrium: The point of equilibrium is where AD and AS intersect.

aggregate demand and supply

The Keynesian long-run aggregate supply curve.

aggregate demand and supply

The new classical long-run aggregate supply curve.

US economy : consumer price and interest rate

US economy : consumer price and interest rate

US economy : real GDP and interest rate

What happens to the interest rate right before recessions (grey area) and what happens during recessions?

US economy : tax revenues and real GDP

How do tax revenues change throughout the economic cycle?

US economy : tax rates and real GDP

How do tax rates change throughout the economic cycle?

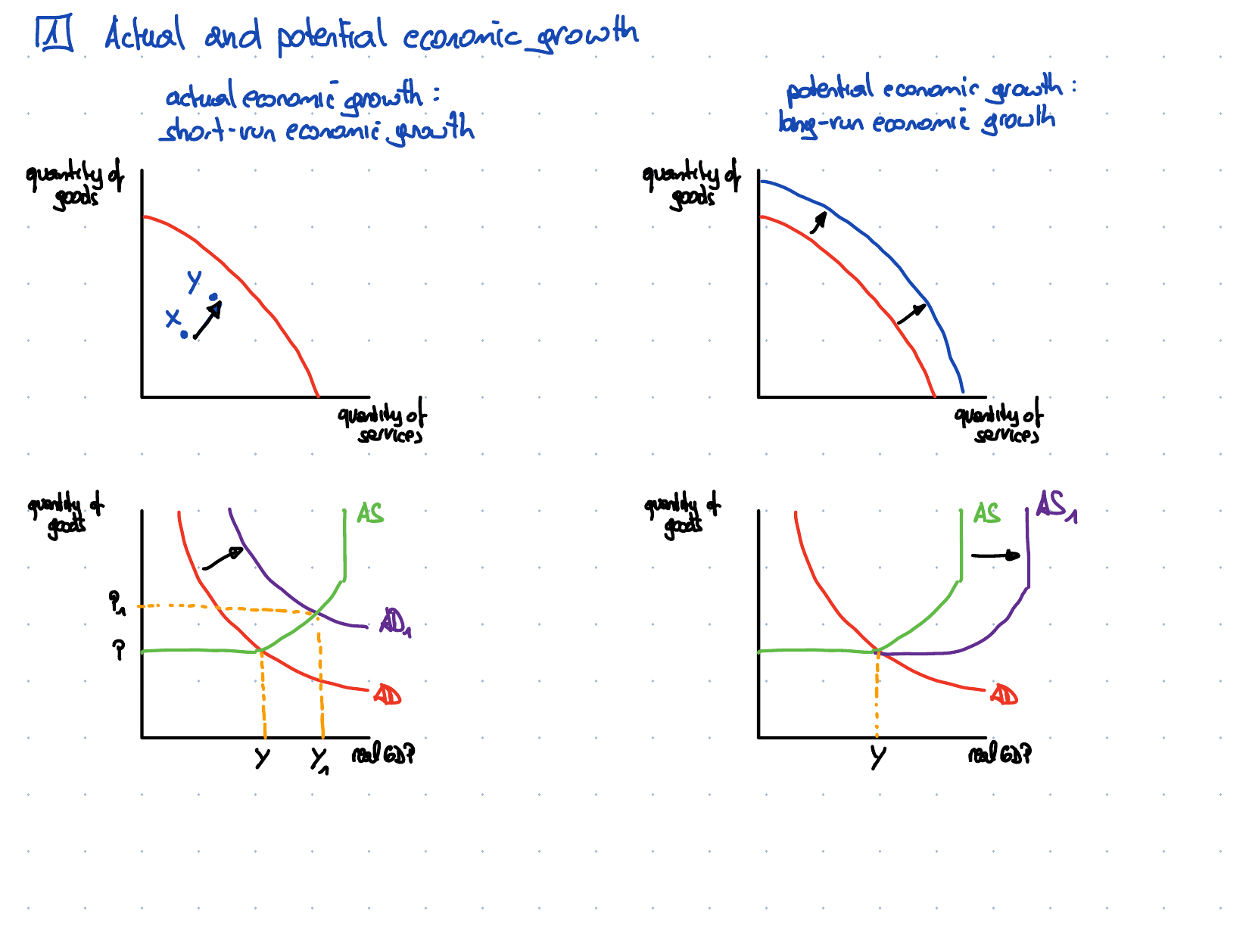

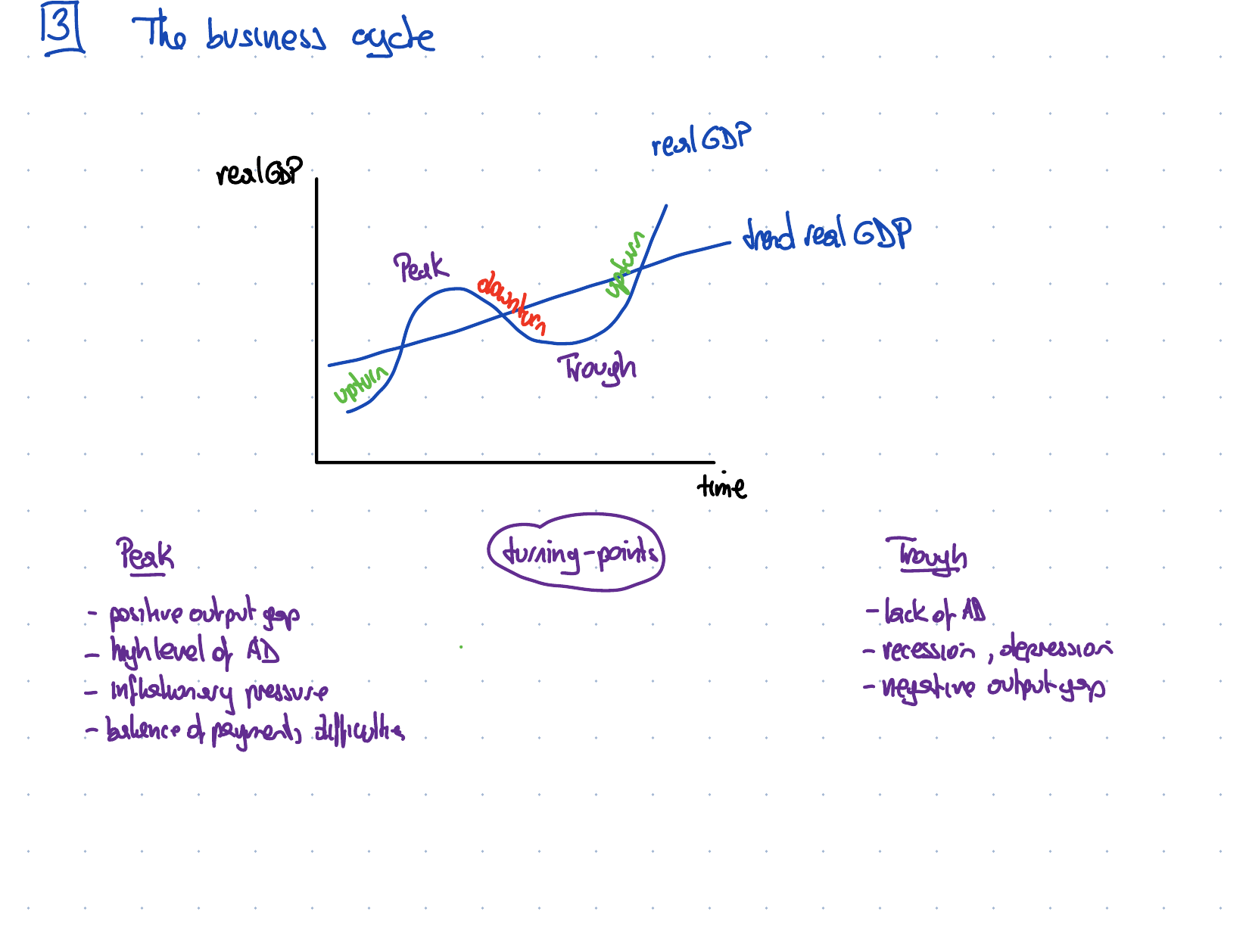

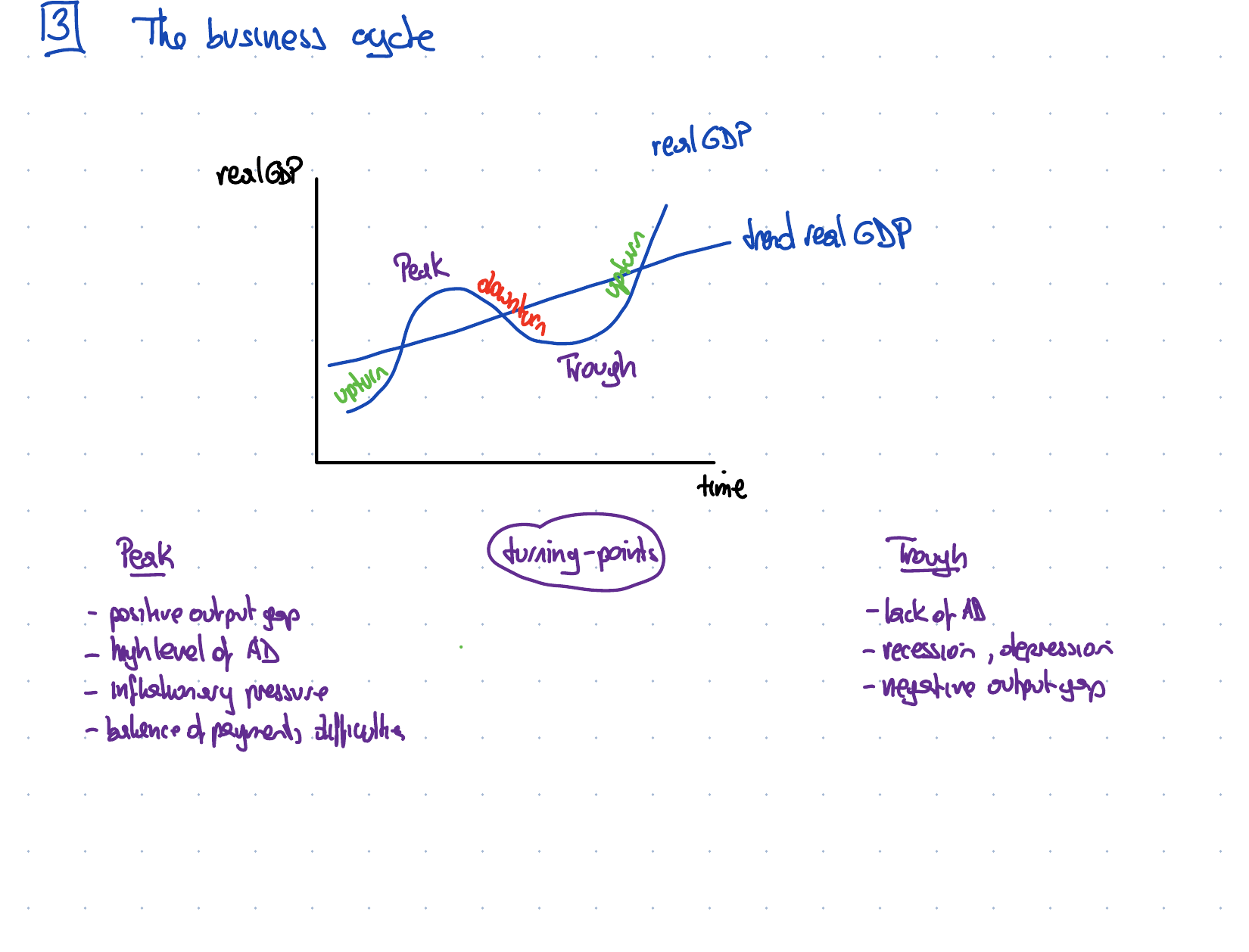

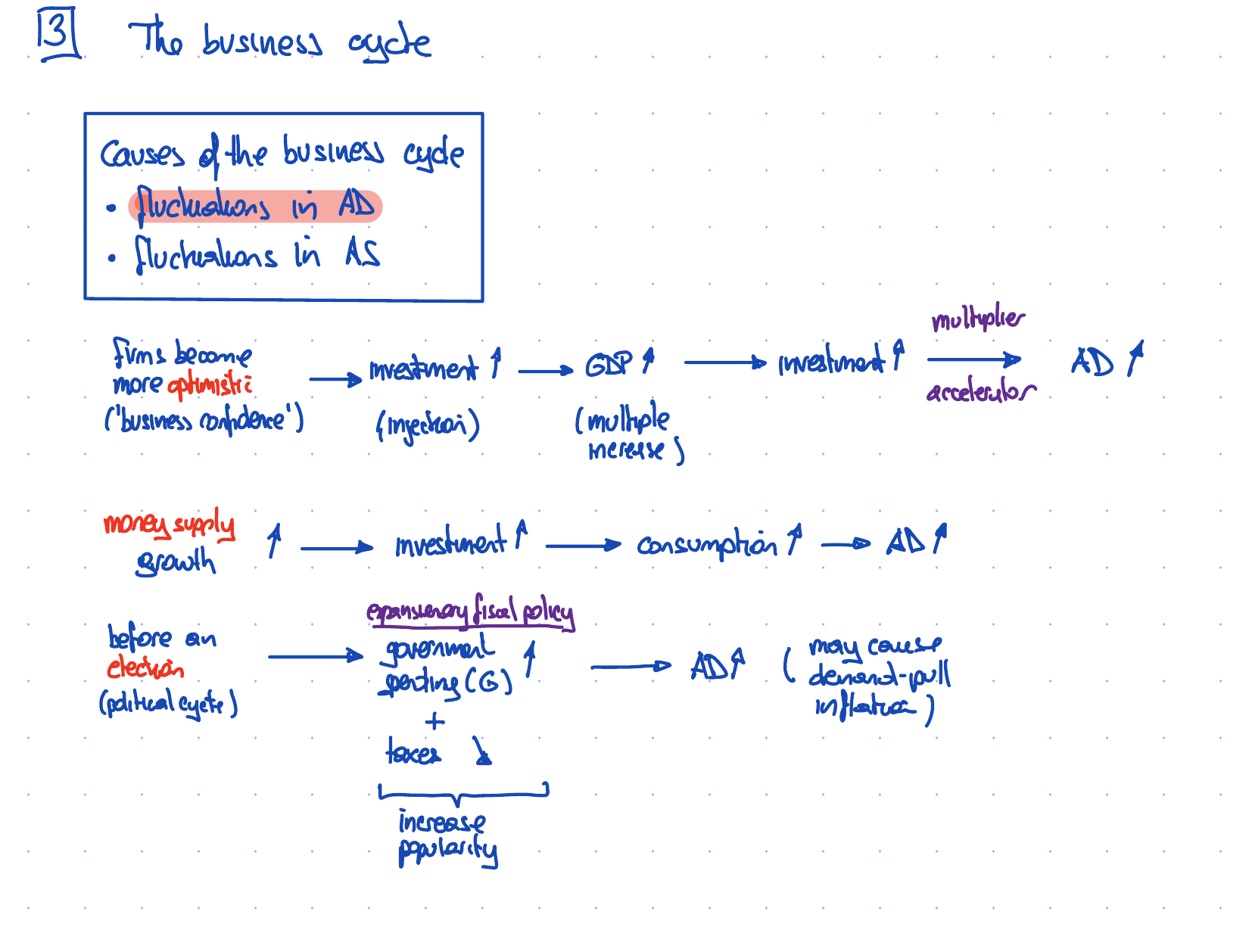

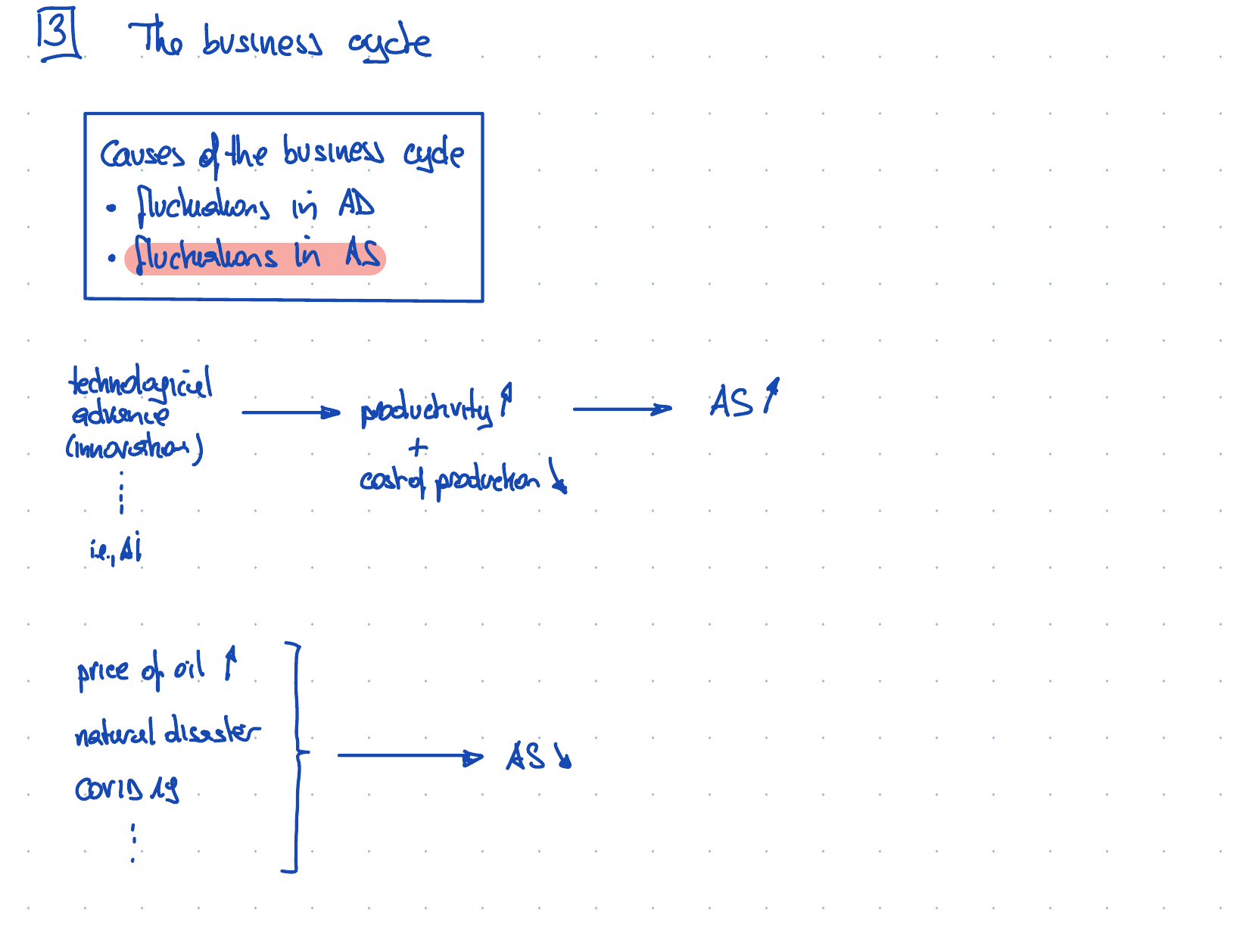

Chapter 18: Economic growth

- economic development

- nominal (or money) GDP

- real GDP

- base year

- constant prices

- price index

- GDP deflator

- efficiency and inefficiency

- recession

- scarcity and choice

Chapter 18: Economic growth

- economic growth

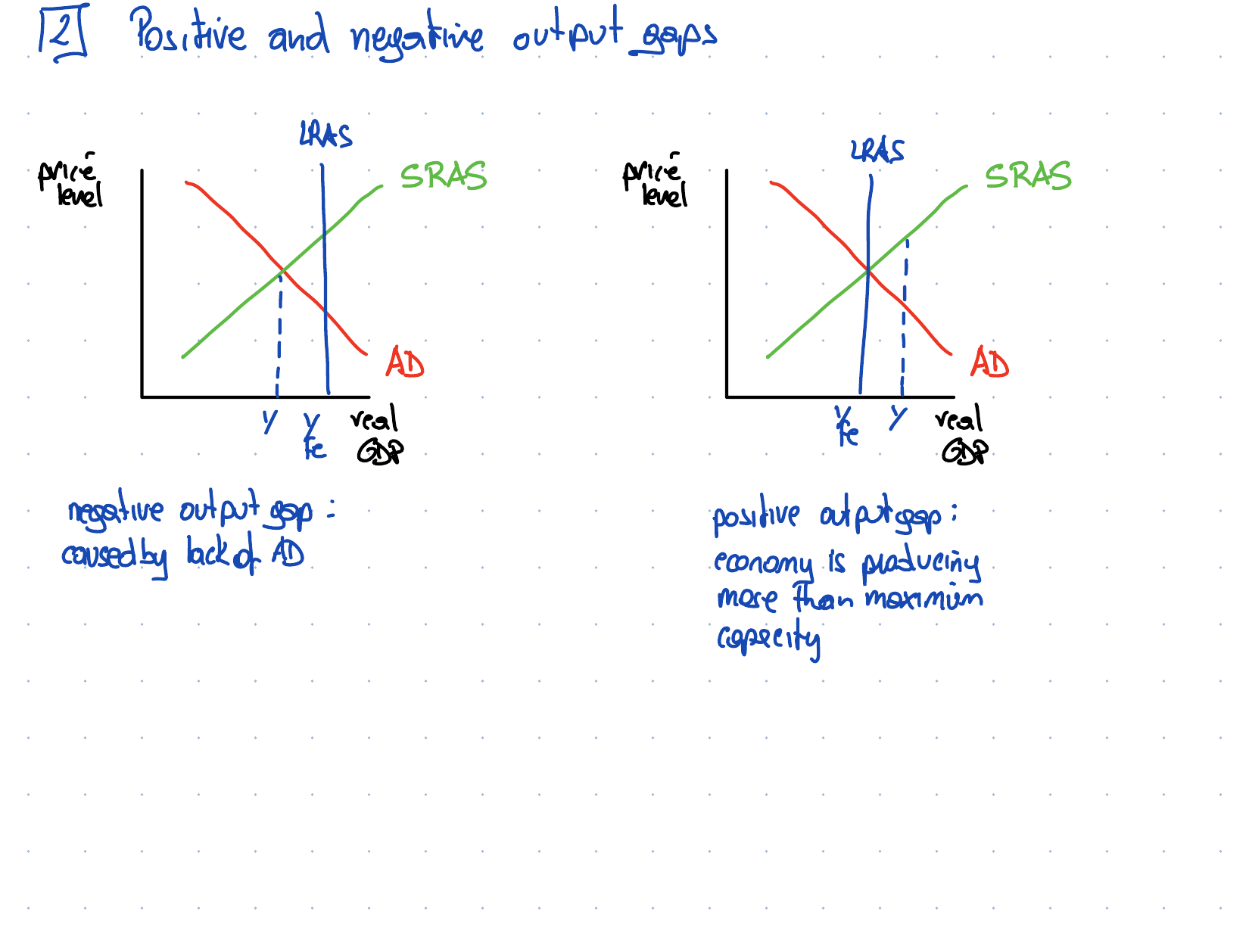

- business cycle (or trade cycle)

- labour-intensive production

- capital-intensive production

Economic growth

economic development

- an increase ...

- ... in welfare and ...

- ... quality of life

nominal (or money) GDP

- total output ...

- ... measured in ...

- current prices

real GDP

- total output ...

- ... measured in ...

- ... constant prices

base year

- the reference point ...

- ... in time.

- it is the starting year ...

- ... in an index and ...

- ... is given a value of 100

constant prices (real prices)

- prices ...

- in a base year

current prices (nominal prices)

- prices ...

- indicated at ...

- ... a given moment in time

price index

- a way of comparing ...

- ... changes in the price level ...

- ... over time.

- the value of the first year ...

- ... in the index (base year) ...

- ... is set at 100 and ...

- ... the value of each following year ...

- ... is a percentage of it.

GDP deflator

- the price index ...

- ... of all domestically produced ...

- ... goods and services.

efficiency and inefficiency

- when an economy ...

- ... is producing ...

- ... inside its PPC, ...

- ... it is inefficiency

recession

- a decline in ...

- ... real GDP ...

- ... over at least ...

- ... two consecutive quarters

GDP Growth Calculation

GDP Growth Rate is calculated by the percentage increase in GDP from one period to the next

\[ \text{GDP Growth Rate (%)} = \left( \frac{\text{GDP}_{\text{current period}} - \text{GDP}_{\text{previous period}}}{\text{GDP}_{\text{previous period}}} \right) \times 100 \]

productive capacity

Inefficieny point.

productive capacity

Increase in productive capacity.

AD/AS diagram

AD and AS curve.

AD/AS diagram

Economic growth resulting from higher aggregate demand (AD).

AD/AS diagram

Economic growth resulting from higher aggregate supply (AS).

Chapter 19: Unemployment

- unemployment

- unemployment rate

- labour force

- working population

- dependency ratio

- participation rate

- claimant count

- labour force survey

Unemployment rate

Labor market

Credit: modification of "Hospital do Subúrbio" by Jaques Wagner Governador/Flickr Creative Commons, CC BY 2.0

Labor Market Example

Technology and Wages: Applying Demand and Supply

A Living Wage: Example of a Price Floor

labour force participation rate

- percentage of ...

- ... the total population of working age ...

- ... who are actually classified as ...

- ... being part of the labour force

level of unemployment

- total number of workers...

- ... who are unemployed

unemployment and employment

- employment rate is the ...

- proportion of the working age population ...

- ... who are in work ...

- ... and not ...

- ... the proportion of labour force in work.

$ \text{unemployment rate} + \text{employment rate} \neq 100\% $

stock vs. flow

- stock: measured at a particular time period

- flow: measured over a period of time period

methods of measuring unemployment

- claimant count measure:

count the registered unemployed (e.g. for benefits) - labour force survey measure:

survey-based by asking people

What are advantages and disadvantages of each method?

causes of unemployment

- frictional unemployment

- structural unemployment

- cyclical unemployment

frictional unemployment

- job-to-job search

- voluntary unemployment

- search unemployment

- casual unemployment

- seasonal unemployment

structural unemployment

- regional unemployment

- technological unemployment

- international unemployment

cyclical unemployment

- demand-deficient unemployment

- AD falls

consequences of unemployment

- workers: income $\downarrow$

- unemployed:

- duration uf unemployment makes it harder to find a new job

- decline in physical and mental health

- firms:

- not faced with wage rises

- lower demand for goods and services

Chapter 20: Price stability

- barter

- price stability

- inflation rate

- inflation

- price level

- creeping inflation

- hyperinflation

- deflation

- disinflation

Chapter 20: Price stability

- annual average method

- year-on-year method

- consumer price index (CPI)

- money values

- real data

- cost-push inflation

- wage-price spiral

- demand-pull inflation

- monetarists

Chapter 20: Price stability

- menu costs

- shoe leather costs

- fiscal drag

- inflationary noise

- total costs

- debtors

Chapter 20: Price stability

- inflation

- creeping inflation

- accelerating inflation

- hyperinflation

- deflation

- disinflation

- general price level

Chapter 20: Price stability

- cost of living

- consumer price index (CPI)

- sampling

- household expenditure

- weights

- base year

- nominal value

Chapter 20: Price stability

- real value

- demand-pull inflation

- monetary inflation

- cost-push inflation

- anticipated inflation

- unanticipated inflation

- imported inflation

Chapter 20: Price stability

- menu costs

- shoe lether costs

- fiscal drag

- stagflation

Inflation of consumer prices

Consumer price index

inflation

- a general increase ...

- ... in the average level of prices ...

- ... in an economy ...

- ... over a period of time

creeping inflation

- a situation where ...

- ... the rate of inflation ...

- ... is reasonably low ...

- ... say about 2%

accelerating inflation

- a situation where ...

- ... the rate of inflation ...

- ... is rising ...

- ... over a period of time

hyperinflation

- a situation where ...

- ... the rate of inflation ...

- ... is becoming very high ...

- ... and is damaging confidence ...

- ... in the country’s economy

deflation

- a general decrease ...

- ... in the average level of prices ...

- ... in an economy ...

- ... over a period of time

disinflation

- a general increase ...

- ... in the average level of prices ...

- ... in an economy ...

- ... over a period of time ...

- ... where the rate of increase ...

- ... is less than ...

- ... in the previous time period

general price level

- the average level of prices ...

- ... of all consumer goods and services ...

- ... in an economy ...

- ... at a given time

cost of living

- the cost of ...

- ... a selection of goods and services ...

- ... that are consumed by ...

- ... an average household ...

- ... in an economy ...

- ... at a given time

consumer price index (CPI)

- a way of measuring changes in the prices ...

- ... of a number of ...

- ... consumer goods and services ...

- ... in an economy ...

- ... over a period of time

sampling

- the use of a representative sample ...

- ... of goods and services ...

- ... consumed in an economy ...

- ... to give an indication of changes ...

- ... in the cost of living

household expenditure

- a survey is taken on ...

- ... a regular basis (usually every month) ...

- ... to record changes in the prices ...

- ... of a selection of goods and services ...

- ... that constitutes a representative basket

weights

- the items in a representative sample ...

- ... of goods and services ...

- ... bought by people in an economy ...

- ... will not all be of the same importance; ...

- weights are given ...

- ... to each of the items ...

- ... to reflect the relative importance ...

- ... of the different components in the basket ...

- ... and so a price index ...

- ... involves a weighted average

base year

- a year chosen so that comparisons ...

- ... can be made over a period of time;

- the base year for an index ...

- ... is given a value of 100

nominal value

- the value of a sum of money ...

- ... without taking into account ...

- ... the effects of inflation

real value

- the value of a sum of money ...

- ... after taking into account (removing) ...

- ... the effects of inflation

demand-pull inflation

- a rise in the ...

- ... general level of prices ...

- ... in an economy ...

- ... caused by too much demand ...

- ... for goods and services

causes of inflation

- cost-push inflation

- demand-pull inflation

consequences of inflation

- costs of inflation

- benefits of inflation

- factors affecting the consequences of inflation

- recent reductions in global inflation

consequences of inflation: costs of inflation

- $(X-M) \downarrow$

- unplanned redistribution of income

- menu costs

- shoe leather costs

- fiscal drag

- discouragement of investment

- inflationary noise

- inflation causing inflation

consequences of inflation: benefits of inflation

- output $\uparrow$

- burden of debt $\downarrow$

- some unemployment $\downarrow $ (pause wage rises)

consequences of inflation: factors affecting

- cause of inflation : demand-pull vs. cost-push

- rate of inflation : high vs. low

- rate of inflation : accelerating vs. stable

- expected vs. unexpected inflation rate

- relative inflation rate to other countries

consequences of inflation: recent reductions in global inflation

- advances in technology : costs $\downarrow$ $\longrightarrow$ AD $\uparrow$

- increased international competition

- changes in the labour market

Causes & consequences of deflation

deflation $\longrightarrow$ burden of debt $\uparrow$

$\longrightarrow$ real rate of interest $\uparrow$ $\longrightarrow$ menu cost

- good deflation : as a result of AS $\uparrow$

price level $\downarrow$ & real GDP $\uparrow$ - bad deflation : as a result of AD $\downarrow$

price level $\downarrow$ & real GDP $\downarrow$

[add diagram]

Extract: How should you fight inflation?

read How should you fight inflation?

by Joseph Stiglitz

aggregate demand and aggregate supply.

Video: Inflation (Bank of England)

Extract: Global Inflation

read Peak inflation? The new dilemma for central banks from FT

Part 5: Government macroeconomic intervention

- Government macroeconomic policy objectives

- Fiscal policy

- Monetary policy

- Supply-side policy

Chapter 21: Government macroeconomic policy objectives

- inflation target

- unemployment

- economic growth

Annual budget of NASA

Central government expenditure as share of GDP

Chapter 22: Fiscal policy

- fiscal policy

- government budget

- budget deficit

- budget surplus

- balanced budget

- national debt

Chapter 22: Fiscal policy

- direct tax

- income tax

- indirect tax

- specific tax

- ad valorem tax

- progressive taxation

Chapter 22: Fiscal policy

- regressive taxation

- proportional taxation

- flat-rate tax

- marginal tax rate

- average tax rate

- canons of taxation

Chapter 22: Fiscal policy

- capital spending (or investment spending)

- current spending

- discretionary fiscal policy

- automatic stabilisers

- expansionary fiscal policy

- contractionary fiscal policy

fiscal policy

- the use of ...

- ... taxation and government spending ...

- ... to influence aggregate demand

budget

- an annual statement ...

- ... in which the government ...

- ... outlines plans for its ...

- ... spending and tax revenue

budget surplus

- government revenue ...

- ... exceeding ...

- ... government expenditure

budget deficit

- government expenditure ...

- ... exceeding ...

- ... government revenue

balanced budget

- government revenue ...

- ... equalling ...

- ... government expenditure

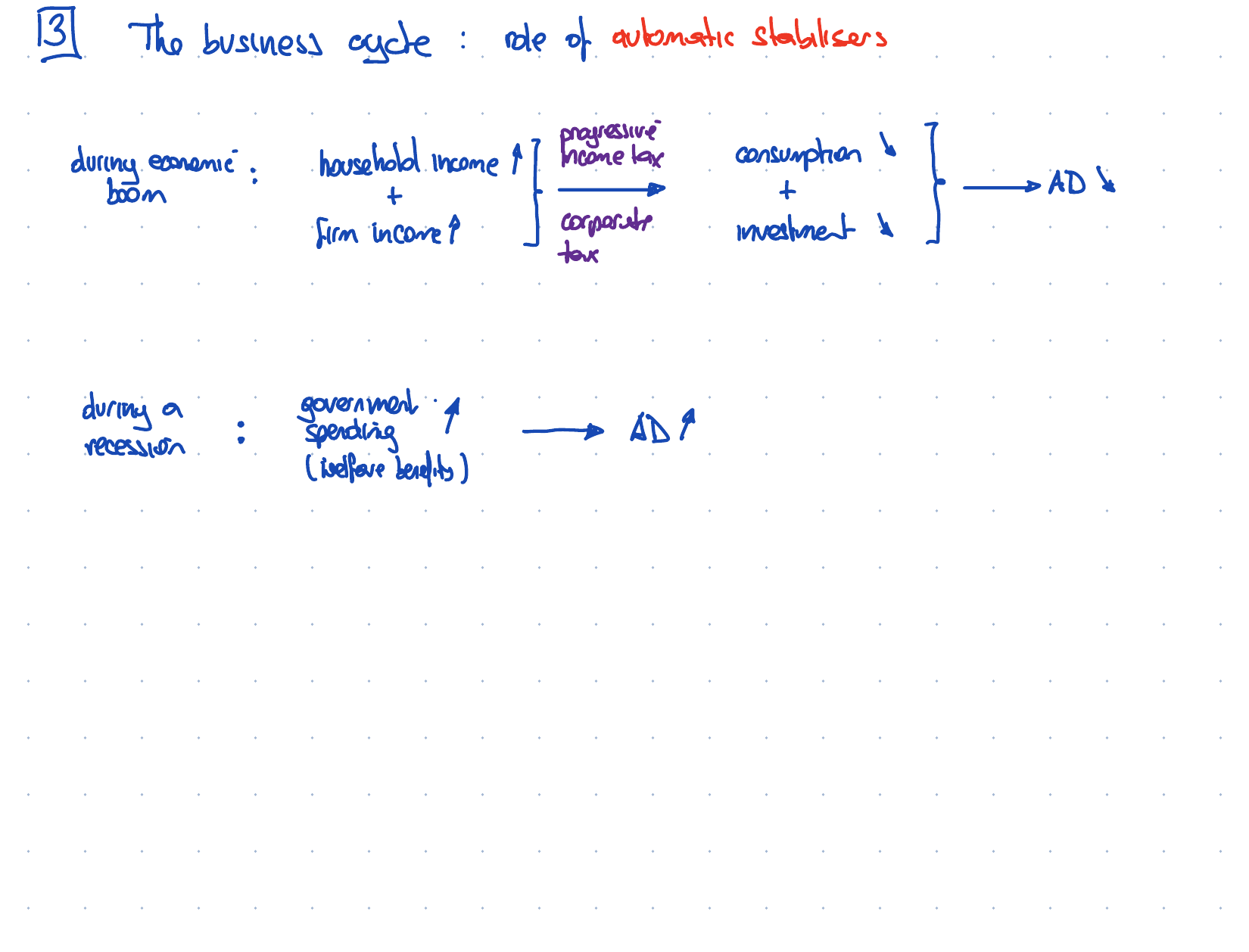

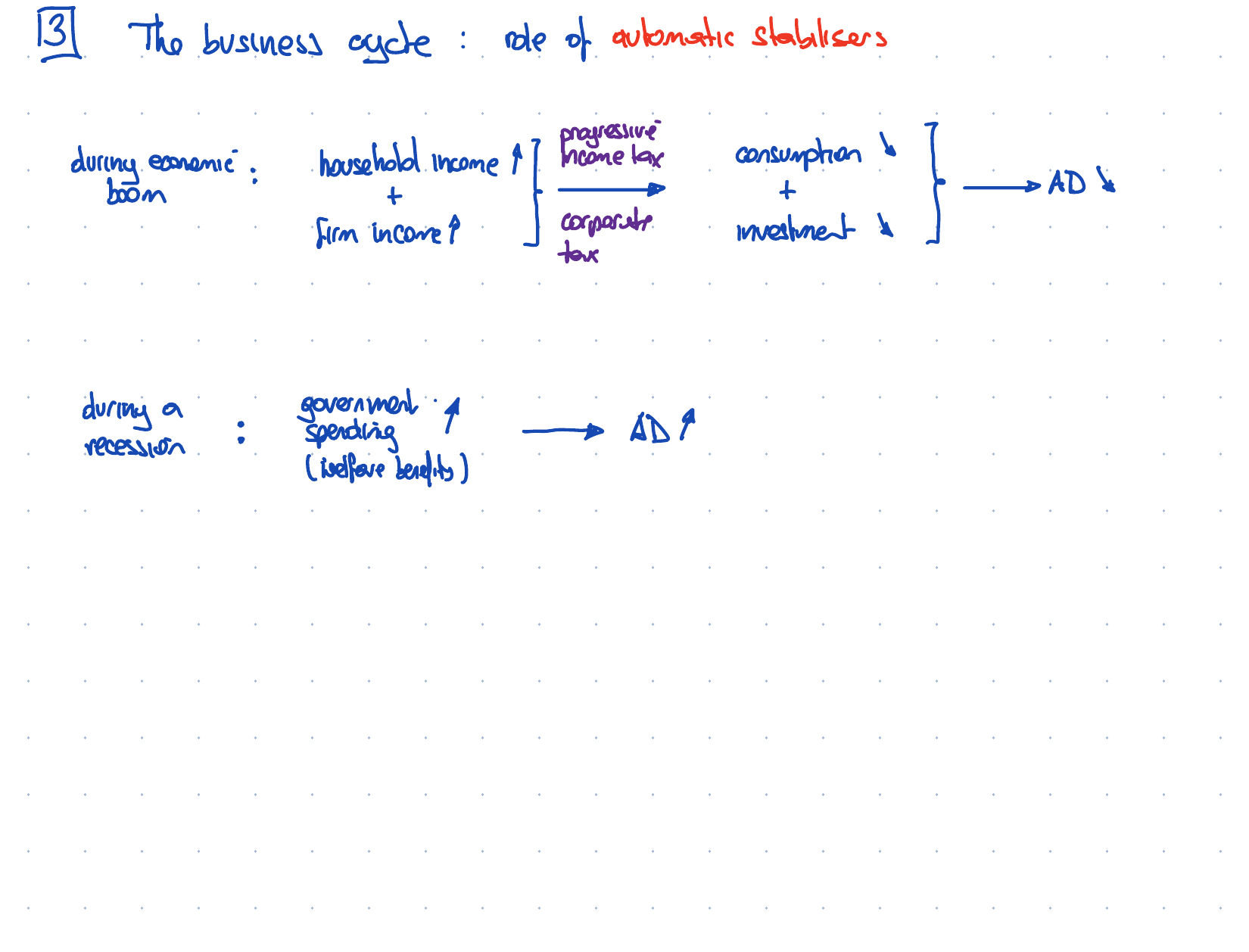

automatic stabilisers

- changes in ...

- ... government spending and taxation ...

- ... that occur to ...

- ... reduce fluctuations ...

- ... in aggregate demand ...

- ... without any alteration ...

- ... in government policy

cyclical budget deficit

- a budget deficit ...

- ... caused by a decline ...

- ... in economic activity

structural budget deficit

- a budget deficit ...

- ... caused by an imbalance between ...

- ... government spending and taxation

tax base

- the coverage of ...

- ... what is taxed

national debt

- the total amount ...

- ... of government debt

specific taxes

- taxes that are charged ...

- ... as a set amount ...

- ... per unit

sin taxes

- taxes on products ...

- ... considered harmful to consumers

direct taxes

- taxes on ...

- ... income and wealth

tax avoidance

- the legal bending ...

- ... of the rules of the tax system ...

- ... to pay less tax

tax evasion

- the illegal non-payment ...

- ... or underpayment of a tax

regressive tax

- a tax which takes ...

- ... a larger percentage ...

- ... of the income or wealth ...

- ... of those on low incomes

proportional tax

- a tax which takes ...

- ... the same percentage ...

- ... of the income or wealth ...

- ... of all income groups

marginal rate of taxation (mrt)

- the proportion of ...

- ... extra income taken in tax

average rate of taxation (art)

- the proportion of income ...

- ... that is taxed

current government spending

- government spending ...

- ... on providing goods and services

capital government spending

- government spending ...

- ... on investment

exhaustive government spending

- government spending ...

- ... which makes use of resources

non-exhaustive government spending

- government spending ...

- ... which allows others to decide ...

- ... how resources are used

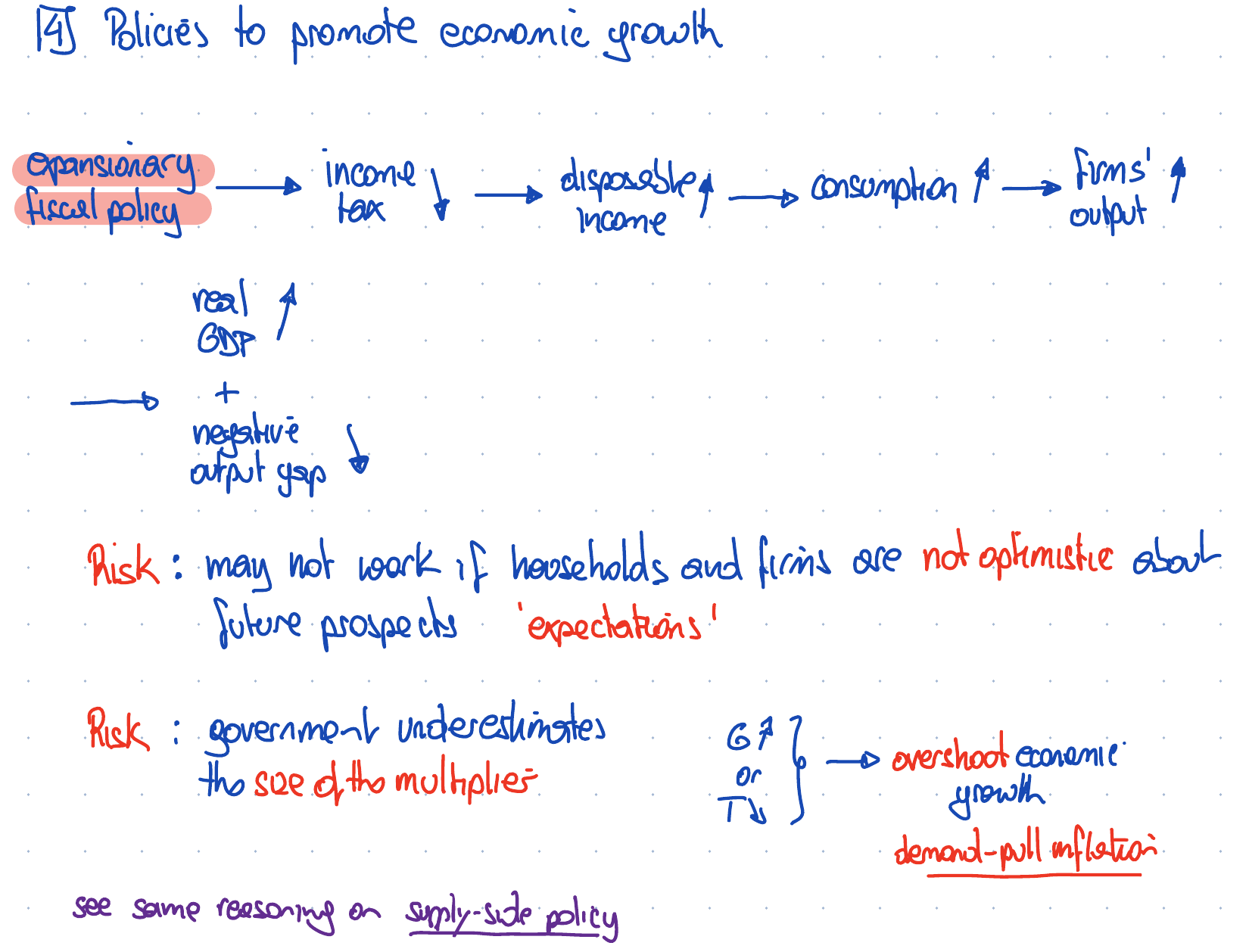

expansionary fiscal policy

- increases in ...

- ... government spending and ...

- ... cuts in taxes ...

- ... designed to increase aggregate demand

contractionary fiscal policy

- decreases in ...

- ... government spending and ...

- ... increases in taxes ...

- ... designed to reduce ...

- ... the growth of aggregate demand

discretionary fiscal policy

- deliberate changes in ...

- ... government spending and taxation

Chapter 23: Monetary policy

- monetary policy

- hot money

- quantitative easing

- open market operations

- expansionary monetary policy

- contractionary monetary policy

Chapter 24: Supply-side policy

- supply-side policy

- productivity

- productive capacity

- labour productivity

Part 6: International economic issues

- The reasons for international trade

- Protectionism

- Current account of the balance of payments

- Exchange rates

- Policies to correct imbalances in the current account of the balance of payments

Chapter 25: The reasons for international trade

- absolute advantage

- comparative advantage

- trading possibility curve

- bilateral trade

- multilateral trade

- globalisation

- specialisation

- free trade

- trade liberalisation

- trade creation

- World Trade Organization

- terms of trade

absolute advantage and comparative advantage

absolute advantage

- the ability to produce a good ...

- ... more efficiently (e.g. with less labour)

comparative advantage

- the ability to produce a good ...

- ... relatively more efficiently ...

- ... (i.e. at lower opportunity cost) ...

comparative advantage : example

comparative advantage : example

comparative advantage : example

comparative advantage : example

comparative advantage : example

comparative advantage : example

comparative advantage : example

comparative advantage : example

law of comparative advantage

- a theory arguing that there may be ...

- ... gains from trade arising ...

- ... when countries (or individuals) ...

- ... specialise in the production of goods ...

- ... or services in which they have ...

- ... a comparative advantage

trading possibilities curve

- shows the consumption possibilities ...

- ... under conditions of free trade

trade liberalisation

- a process of moving towards ...

- ... freer trade by ...

- ... removing restrictions on trade

terms of trade

- the ratio of ...

- ... export prices to ...

- ... import prices

income terms of trade

- the value of a ...

- ... country's exports ...

- ... divided by the ...

- ... price of its imports.

- measures the purchasing power ...

- ... of a country's exports in terms of ...

- ... the price of its imports

bilateral trade

- where trade takes place ...

- ... between two countries

multilateral trade

- where trade takes place ...

- ... between a number of countries

globalisation

- the process whereby there is ...

- ... an increasing world market ...

- ... in goods and services ...

- ... making an increase in multilateral trade ...

- ... more likely

specialisation

- the process whereby ...

- ... individuals, firms and economies ...

- ... concentrate on producing those products ...

- ... in which the have an advantage

free trade

- trade that is not restricted ...

- ... or limited ...

- ... by different types of ...

- ... import or export control

trade liberalisation

- the removal or reduction ...

- ... of restrictions or barriers ...

- ... to the free exchange of ...

- ... goods and services ...

- ... between countries

trade creation

- the creation of new trade ...

- ... as a result of ...

- ... the reduction or elimination ...

- ... of trade barriers

terms of trade

- the price of a ...

- ... country's exports in relation to ...

- ... the price of the country's imports

$$ \small\frac{ \text{index number showing the average price of exports} }{ \text{index number showing the average price of imports} } \times 100 $$

$\longrightarrow$ check data at OECD

$\longrightarrow$ check commodities TOT at IMF

causes of changes in the terms of trade

- demand for and supply of exports and imports

- inflation rate

- exchange rate

Prebisch-Singer hypothesis

- IED of manufactured goods

is far greater than

IED of primary products

- as income rises ...

- ... the demand for manufactured goods ...

- ... increase more than ...

- ... the demand for primary products

benefits of specialisation and free trade

- efficient allocation of resources

- factor endowment

- lower prices & better quality

- higher output

- economies of scale

- choice of products

- ...

- ... ...

- ... ...

- ... ...

- ...

Chapter 26: Protectionism

- protectionism

- tariff

- absolute poverty

- quota

- embargo

- voluntary export restraint

- exchange control

- infant industries

- dumping

- monopoly

- current account

Chapter 26: Protectionism

- absolute advantage

- protectionism

- tariff

- import duty

- quota

- export subsidy

- exchange controls

Chapter 26: Protectionism

- embargo

- voluntary export restraint (VER)

- infant industry argument

- sunrise industries

- sunset industries

- dumping

protectionism

- protecting domestic producers ...

- ... from foreign competition

tariff

- a tax imposed ...

- ... on imports

absolute poverty

- a condition where ...

- ... people's income ...

- ... is too low ...

- ... to enable them ...

- ... to meet their basic needs

quota

- a limit ...

- ... on imports

embargo

- a ban ...

- ... on imports and/or exports