Business

2iec

Structured Writing - Simple Model

Structured Writing - Intermediate Model

Structured Writing - Advanced Model

Learner Guide

Check the Learner GuidePart 1: Business and its environment

- Enterprise

- Business structure

- Size of business

- Business objectives

- Stakeholders in a business

Chapter 1: Enterprise

- business objectives

- transformation process

- factors of production

- primary sector

- adding value

- brand

- market forces

- opportunity cost

- entrepreneur

- enterprise

- intrapreneur

Chapter 2: Business structure

- nationalisation

- privatisation

- merit goods

- unlimited liability

- company

- shareholders

- limited liability

- franchise

- co-operatives

- joint ventures

- social enterprises

Chapter 3: Size of business

- niche

- type of integration (horizontal, vertical, conglomerate diversification)

- internal and external growth

Chapter 4: Business objectives

- objective

- labour productivity

- corporate objective

- market share

- cash flow

- ethics

- social responsibility

Chapter 4: Business objectives

- mission statement

- aim

- strategy

- tactics

- target

- budgets

- ethical behaviour

Chapter 5: Stakeholders in a business

- stakeholders

- authority

- internal stakeholders

- external stakeholders

- dividends

Chapter 6: External influences on business activity

- Political and legal influences

- Social and demographic influences

- Technological influences on business activities

- Influence of competitors and suppliers

- International influences

- Environmental influences on business activity

1. Political and legal influences

- privatisation or nationalisation

- legal constraints

- conditions of work, minimum wage, ...

- competition

- ...

- health and safety laws

- ...

activity 6.1

activity 6.2

activity 6.3

activity 6.4

2. Social and demographic influences

- corporate social responsibility (CSR)

- demographic changes

- ...

3. Technological influences on business activities

- technological change

- impact on decision-making of businesses

- process of introducing technology into a business

4. Influence of competitors and suppliers (short)

- market share

- market power

- decision on pricing

- ...

5. International influences

- international trade (importance, agreements, ...)

- WTO, Free-trade blocs

- technology in international trade

- AI

- blockchain

- digital payments

- Multinational businesses

- ...

6. Environmental influences on business activity

- CSR, environment and business decisions

- environmental audits

- sustainability

- ...

analyse ...

analyse ...

Chapter 7: External economic influences on business activity

- Government support for business activity

- How governments deal with market failure

- Macroeconomic objectives of governments

- How economic objectives and performance impact business activity

- Government policies to achieve macroeconomic objectives

Government support for business activity

- Government assistance for entrepreneurs

- loan guarantee schemes

- provide information, advice, training, ...

- financing of workshops, ...

- reduce paperwork and legal formalities

- reduce corporation tax on new and small businesses

- Government assistance for all businesses

Government support for business activity

- Government assistance for entrepreneurs

- Government assistance for all businesses

- subsidies to keep prices down

- subsidies to protect employment

- grants to relocate to areas with high unemployment

- financial support for housing

Government support for business activity

advantages and disadvantages of subidies

- advantages

- avoids business failure

- keeps suppliers in business

- avoids rising imports

- disadvantages

- taxes will rise

- disincentive to be more efficient

- consumers drawn to subsidised products

How governments deal with market failure

- Examples of market failure

- external costs

- labour training

- monopoly producers

- Correcting or controlling market failure

Macroeconomic objectives of governments

- economic growth

- inflation

- unemployment

- balance of bayment

- exchange rate

How economic objectives and performance impact business activity

- Economic growth

- benefits

- causes

- business cycle

- role of recessions

- inflation and deflation

- Unemployment

How economic objectives and performance impact business activity

- Economic growth

- inflation and deflation

- causes of inflation

- impact of low inflation

- impact of high inflation

- Unemployment

How economic objectives and performance impact business activity

- Economic growth

- inflation and deflation

- Unemployment

- causes of unemployment

- cyclical unemployment

- structural unemployment

- frictional unemployment

- costs of unemployment

Government policies to achieve macroeconomic objectives

- Monetary policy

- Fiscal policy

- Supply-side policies

- Exchange rate policy

Chapter 8: Business strategy

- Business strategy : meaning and purpose

- Strategic management: meaning and purpose

- Approaches to developing business strategy

Business strategy : meaning and purpose

- Establishing business strategy

- Resources available

- Strengths of the business

- Competitive environment

- Objectives

Strategic management: meaning and purpose

- Strategic choice

- Strategic implementation

- Strategy and tactics

- The need for strategic management

Approaches to developing business strategy

- Blue ocean strategy

- Scenario planning

- SWOT analysis

- PEST analysis

- Porter's five forces analysis

- Core competencies

- The Ansoff matrix

- Force-field analysis

- Decision trees

essay questions

- Evaluate how a large supermarket company might use SWOT and PEST analysis in order to make a successful expansion overseas.

- Evaluate why a hotel business might use blue ocean strategy, rather than concentrating on red ocean strategy.

- Evaluate how a fast-food company might use Porter's Five Force analysis to identify changes to the market environment in which they operate.

essay questions

- Evaluate whether a retail clothing business without identifiable core competencies might fail in the market in your country.

- Evaluate how a wheat-farming business might use the Ansoff Matrix and decision-tree analysis to decide whether to move into chicken farming or use the land to build and rent holiday accommodation to tourists.

Part 2: Human resource management

- Human resource management

- Motivation

- Management

Chapter 10: Human resource management

- human resource management (HRM)

- delayering

- teamworking

- workforce plan (or human resource plan)

- labour turnover

- recruitment and selection

- job descriptions

- person specifications (or job specifications)

- employment contract

Chapter 10: Human resource management

- business culture

- dismissal

- redundancies

- employee welfare

- employee morale

- work-life balance

- diversity

- equality

Chapter 10: Human resource management

- training

- development

- delegation

- intrapreneurship

- multi-skilling

- trade union

- collective bargaining

Chapter 10: Human resource management

\[\begin{aligned} \text{turnover} & = \frac{ \text{number of staff leaving during the year} }{ \text{average number of staff} } \times 100 \end{aligned} \]

Chapter 11: Motivation

- motivation

- absenteeism

- human needs

- schools of thought

- piece-rate

- division of labour

- hierarchy of needs

- hygiene factors ( or maintenance factors)

- motivators

Chapter 11: Motivation

- performance-related pay (PRP)

- variable pay

- fringe benefits (or perks)

- job redesign

- job enrichment (or vertical loading)

- job enlargement (or horizontal loading)

- job rotation

- empowerment

- job design

- employee participation

Chapter 12: Management

- leadership

- management

- autocratic management (or authoritarian management)

- paternalistic management

- democratic management (or participative management)

- laissez-faire management

Part 3: Marketing

- The nature of marketing

- Market research

- The marketing mix - product and price

- The marketing mix - promotion and place

Chapter 17: The nature of marketing

- marketing

- marketing objective

- corporate objective

- marketing strategy

- business-to-consumer marketing (B2C)

- business-to-business marketing (B2B)

- market size

Chapter 17: The nature of marketing

- market growth

- unique selling point (USP)

- niche marketing

- market segment

- mass marketing

- customer-relationship marketing (CRM)

- customer retention

Chapter 17: The nature of marketing

\[\begin{aligned} \text{market share} & = \frac{ \text{sales of a business (or product)} }{ \text{total market sales} } \times 100 \\ \\ \text{market growth} & = \frac{ \text{(market sales)}_{ \text{this year} } - \text{(market sales)}_{ \text{last year} } }{ \text{market sales}_{ \text{last year} } } \times 100 \end{aligned} \]

Chapter 18: Market research

- market research

- primary market research

- focus group

- secondary market research

- sample

- validity of market research

- reliability of market research

Chapter 18: Market research

\[\begin{aligned} \text{market growth} & = \frac{ \text{change in market size} }{ \text{original market size} } \times 100 \\ \\ \text{market share of business} & = \frac{ \text{sales by the business} }{ \text{total market sales} } \times 100 \end{aligned} \]

Chapter 19: The marketing mix - product and price

- marketing mix

- products

- tangible attributes

- intangible aspects

- product differentiation

- product portfolio analysis

- product life cycle

- extension strategy

- product portfolio analysis (PPA)

Chapter 19: The marketing mix - product and price

- Boston Matrix

- competitive pricing

- penetration pricing

- price skimming

- price discrimination

- dynamic pricing

- cost-based pricing

- psychological pricing

- promotional mix

Chapter 20: The marketing mix - promotion and place

- digital promotion

- click-through rate (CTR)

- marketing expenditure budget

- distribution channel

- distribution outlet

The Economics of Aldi

strategies that Aldi uses to maintain low prices and attract customers

The Economics of Aldi

discuss the following items

- Store Layout and Size

- Limited Product Range and Simplified Operations

- Cost-Cutting Measures

- Marketing and Customer Perception

- Known Value Items

- Private Label Products

- Recession and Growth

- Expansion and Competition

- Target Audience

Part 4: Operations management

- The nature of operations

- Inventory management

- Capacity utilisation and outsourcing

Chapter 23: The nature of operations

- output

- inventory

- operations mangement

- productivity

- sustainable

- capital-intensive

- labour-intensive

- marketing function

$\longrightarrow$ identify opportunities within a market - operations function

$\longrightarrow$ deliver as effectively as possible

effective operations

- means the business ...

- ... is meeting its operational targets

efficient operations

- produce and deliver products ...

- ... in a cost-efficient manner

consequences of poor operations

- mistakes are being made during production

- items will have to be replaced

- products have to be recalled

- damages have to be paid

output

- the total amount produced ...

- ... in a given time period

different forms of the transformation process

involves changing the ...- ... characteristics of

- materials

- information

- customers

- ... location of materials and information

- ... ownership of materials

inventory

- refers to the stocks held in a business ...

- ... such as materials ...

- ... and semi-finished goods

operations mangement

- overseeing ...

- ... the planning, coordination and control

- ... of the transformation process, ...

- ... turning resources (inputs) into outputs.

factors of production

- land

- labour

- capital

- enterprise

labour productivity

\[\begin{aligned} \text{labour productivity} & = \frac{ \text{total output} }{ \text{number of employees} } \times 100 \end{aligned} \]

productivity

- measures the output per hour, ...

- ... per person ...

- ... or per machine.

sustainable activities

- activities that meet the needs of ...

- ... the business or of society ...

- ... without compromising on the ability ...

- ... to meet future needs.

capital-intensive production

- production where there is ...

- ... a high proportion of capital ...

- ... used relative to ...

- ... other factors of production.

labour-intensive production

- production where there is ...

- ... a relatively high proportion ...

- ... of labour used relative to ...

- ... other factors of production.

production process

- factors of production

- land

- labour

- capital

- enterprise

- stages of production :

input $\longrightarrow$ production process $\longrightarrow$ output - operations can increase the added value

operations can increase added value by managing

- efficiency of production

- quality of goods & services

- flexibility & innovation of processes

- design of the product

- efficiency of operations

- effective branding of the product

$\longrightarrow$ production costs $\downarrow$

$\longrightarrow$ quality of goods $\uparrow$

$\longrightarrow$ flexibility of production $\uparrow$

productivity

- high productivity $\longrightarrow$ competitiveness $\uparrow$

- measuring productivity

\[\begin{aligned} \text{labour productivity} & = \frac{ \text{total output} }{ \text{number of employees} } \times 100 \end{aligned} \]

productivity can be increased by

- improving training of employees

$\longrightarrow$ skill level $\uparrow$ - improving worker motivation

- purchasing new technologies

- guaranteeing more efficient management

high productivity : no guarantee for success!

- how popular is the product?

- highly productive workers $\longrightarrow$ wages $\uparrow$

- resistence by workers to measures

- culture of management

- efficiency $\neq$ effectiveness

sustainable operations

- energy use $\downarrow$ & carbon emissions $\downarrow$

- use of non-biodegradable material $\downarrow$

- use of recycled material $\uparrow$

- products that is recyclable

labour intensive operations

- advantages

- interesting job

- low reliance on machines

- meet customer requirement

- disadvantages

- low output

- skilled labour required

- quality not always uniform

labour intensive operations

capital intensive operations

- advantages

- economies of scale

- consistent quality

- low unit cost

- mass production

- disadvantages

- high fixed costs

- high maintenance costs

- keep up with technology changes

capital intensive operations

types of operations methods

- job production : one-off production

- batch production : move from one stage of process to another

- flow production : large scale production

- mass customisation : large scale production with flexibility

job production

batch production

flow production

factors influencing the choice of production method

- size of market

- availability of capital

- availability of other resources

- unskilled workers $\rightarrow$ mass production

- flat area land $\rightarrow$ mass production

- customer requirements

Chapter 24: Inventory management

- supply chain

- supply chain management

- lean production

operations efficiency & inventory

- holding cost $\leftrightarrow$ cost of running out of supplies

- reasons for holding inventory

- raw materials & components (as input)

- work in progress

- finished goods (until being sold)

operations efficiency & inventory

- problems rising from insufficient inventory

- unforseen changes in demand

- obsolete inventories

- inventory wastage

- opportunity costs

- late deliveries

cost & benefit of holding inventory

- cost of holding inventory

- opportunity cost

- storage cost

- wastage & obsolescence

- benefit of holding inventory

- risk of lost sales $\downarrow$

- allows continuous production

- need for special orders from suppliers $\downarrow$

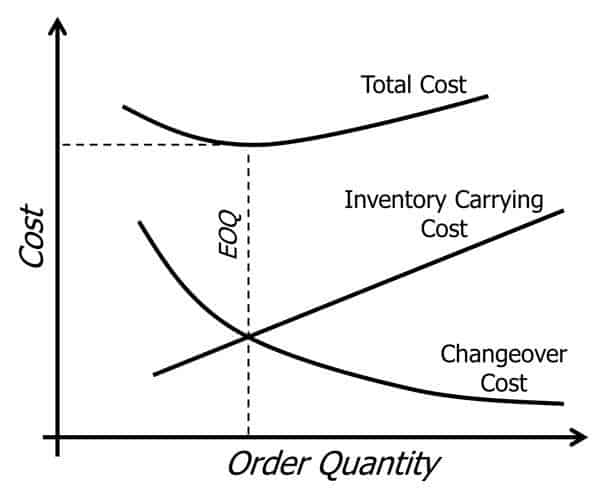

total inventory-holding cost

- economic order quantity (EOQ)

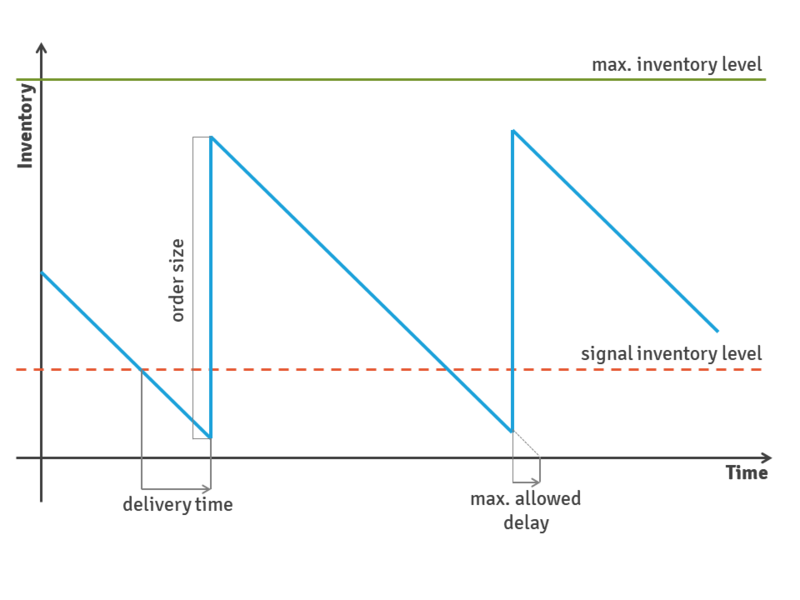

inventory control chart

- monitor a firm's inventory position

- helps to determine the

- appropriate order time and

- order quantity

- key features of inventory control chart

- buffer inventories

- maximum inventory level

- re-order quantity

- lead time

- re-order level

inventory control chart

supply chain management

- goal of supply chain management

- minimize costs and

- improve customer service

- reduce time to convert raw material into completed product

- benefits of supply chain management

- improves customer service

- reduces operating costs

- umproves profitability

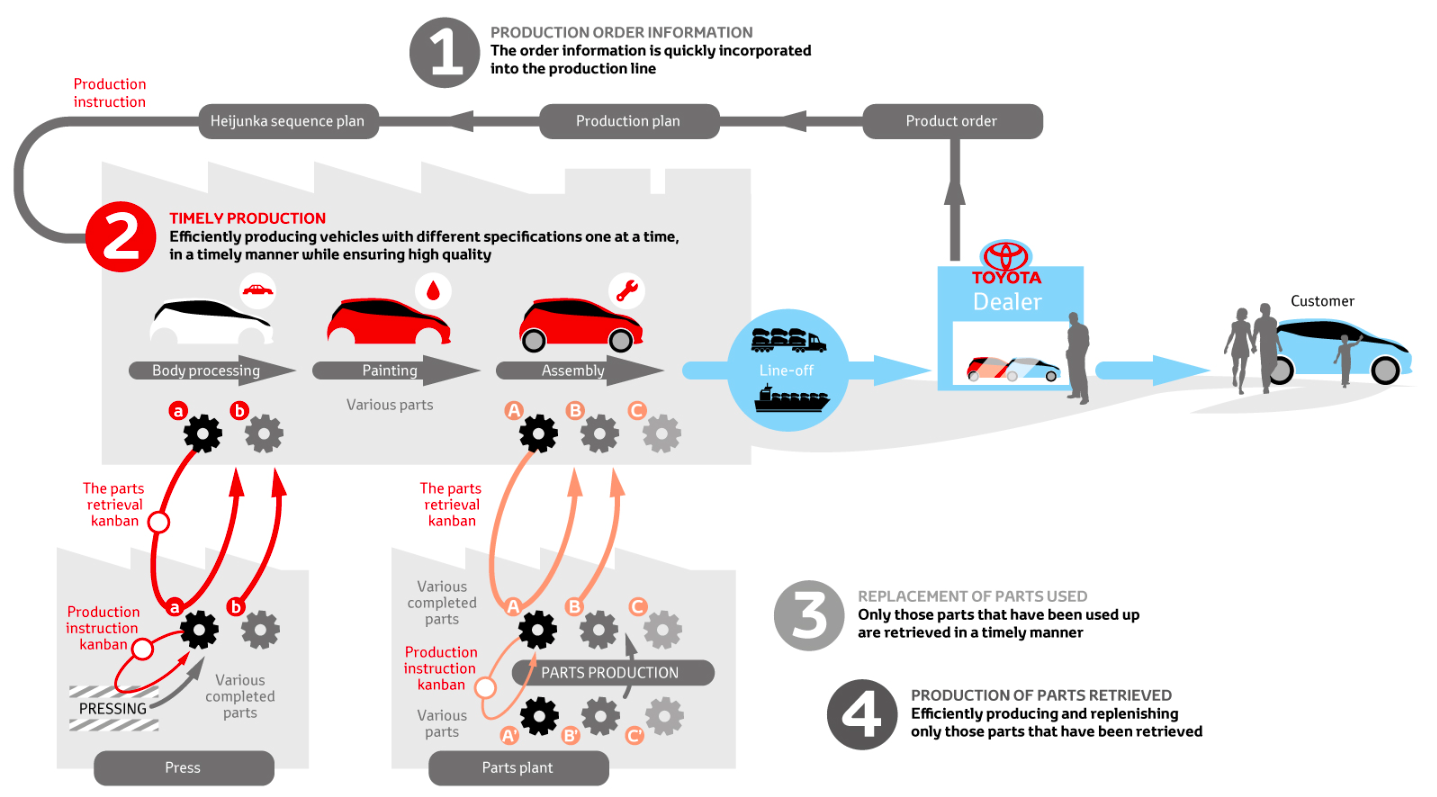

just-in-time model (applied to Toyota)

just-in-time

- advantages

- capital invested in inventory $\downarrow$

- storage cost $\downarrow$

- risk of obsolescence of inventory $\downarrow$

- multi-skilled and adaptable staff

- disadvantages

- delay in supplies $\rightarrow$ production delays

- delivery costs

- many small orders $\rightarrow$ administration cost

- reputation may depend on outside firms

just-in-time model and COVID

source: Supply chains: companies shift from 'just in time' to 'just in case' (FT)

conditions for successful JIT

- good supplier relationships

- skilled and flexible production staff

- flexible machinery

- accurate demand forecasts

- modern IT equipment

- excellent employer-employee relationships

Chapter 25: Capacity utilisation and outsourcing

- capacity

- factors of production

- capacity utilisation

- capacity under-utilisation

- rationalisation

- subcontracting

- outsourcing

Chapter 25: Capacity utilisation and outsourcing

\[\begin{aligned} \text{per cent capacity} & = \frac{ \text{existing output}_{ \text{over a given time period} } }{ \text{maximum possible output}_{ \text{over a given time period} } } \times 100 \end{aligned} \]

Part 5: Finance and accounting

- Business finance

- Forecasting and managing cash flows

- Costs

- Budgets

Chapter 29: Business finance

- asset

- capital

- non-current assets

- short-term sources of finance

- long-term sources of finance

- insolvency

- liabilities

- bankruptcy

- liquidation

Chapter 29: Business finance

- administration

- working capital

- current assets

- trade payables

- trade receivables

- revenue expenditure

- capital expenditure

- statement of financial position

- income statement

asset

- an item owned by a business ...

- ... that can generate an income for the enterprise

- Examples:

- supply of raw material

- machinery

capital

- money invested into a business ...

- ... either by its owners or by other organisations

- Examples:

- money

- machinery

- building

non-current assets

- assets ...

- ... that a business expects to hold for one year or more

- Examples:

- property

- vehicles

sources of finance

- short-term sources of finance : needed for limited period of time (< 1 year)

- long-term sources of finance : needed over a long period of time (> 1 year)

insolvency

- debts (of the business) > assets (available)

- business is unable to pay its debts

liabilities

- money owned by a business ...

- ... to individuals, suppliers, banks, ...

working capital

- money used to pay for day-to-day expenses ...

- ... so the business can keep operating

current assets

- are items owned by a business ...

- ... that can be readily turned into cash

- Examples :

- cash in bank

- trade and other receivables due to settle their accounts soon

- inventories - raw materials and components

current liabilities

- debts payable in short term

- debts repayable to the bank (i.e. overdraft)

- trade and other payables who expect to be paid in the near future

- tax due to authorities

working capital

\[\begin{aligned} \text{working capital} & = \text{current assets} - \text{current liabilities} \end{aligned} \]

bankruptcy

- when an individual, a sole trader or a partnership ...

- ... is judged unable to pay its debts ...

- ... by a court of law

liquidation

- is the dissolution of a company ...

- ... by selling its assets to settle its liabilities

administration

- is a process available to a company ...

- ... to protect itself ...

- ... while it attempts to pay its debts ...

- ... and escape insolvency

trade payables

- is the amount of money ...

- ... owed by a business to its suppliers ...

- ... for goods and services ...

- ... that have been received ...

- ... but which have not been paid for

trade receivables

- is the amount of money ...

- ... owed by a business' customer ...

- ... for products ...

- ... that have been supplied ...

- ... but for which payment has not yet been made

revenue expenditure

- refers to the purchase of items ...

- ... that will be used up within a short space of time

- Examples :

- fuel

- raw materials

capital expenditure

- is the spending by a business ...

- ... on non-current assets

- Examples :

- premises

- production equipment

- vehicles

statement of financial position (balance-sheet)

- is a financial statement ...

- ... that records the assets (possessions) and liabilities (debts) of a business ...

- ... on a particular day ...

- ... at the end of an accounting period

- Example : Luxair (p.56-59)

income statement

- is a financial statement ...

- ... showing a business' sales revenue ...

- ... over a trading period ...

- ... and all the relevant costs incurred to generate that revenue

- Example : Luxair (p.60)

income statement

- is a financial statement ...

- ... showing a business' sales revenue ...

- ... over a trading period ...

- ... and all the relevant costs incurred to generate that revenue

- Example : Luxair (p.60)

Classroom activity

- Read Mobile Phone extract (p.488)

- Analyse the likely increase in working capital from this expansion.

- Discuss how inventories, trade payables and trade receivables could be managed to reduce the need to increse working capital.

- see Learner Guide for the command words

Homework

- Read chapter 29 for next week.

- Revise using the Exam-Style Questions

need for business finance

- why?

start-up capital, working capital, R&D, buy other companies, survival of company - short-term vs. long-term need

buy inventory before busiest months (ST), buy equipment and buildings (LT) - cash $\neq$ profit

cash is needed in the short-run, profit can wait for the long-run

need for business finance

- administration business fails due to a lack of finance

- bankruptcy accountants are appointed to keep the business operational and find a buyer for it - if they fail we have bankruptcy

- liquidation a legal process will begin that will liquidate the assets of the business

working capital

Chapter 30: Forecasting and managing cash flows

- cash flow

- insolvent

- cash flow forecast

- cash inflow

- cash outflow

- net cash flow

Chapter 30: Forecasting and managing cash flows

- opening cash balance

- closing cash balance

- credit control

- bad debt

- overtrading

- decision-making

cash flow

- the sum of ...

- ... cash payments ...

- ... to a business ...

- ... less ...

- ... the sum of ...

- ... cash payments ...

- ... from the business

$ \text{net cash} = \text{total cash inflows} - \text{total cash outflows} $

insolvent

- when a business ...

- ... cannot meet ...

- ... its short-term debts

cash flow forecast

- an estimate ...

- ... of the future ...

- ... cash inflows and outflows ...

- ... of a business

- cash inflow: cash payments into a business

- cash outflow: cash payments out of a business

cash inflows examples

- owner's own capital

- bank loan

- customer's cash purchases

- trade receivables

cash outflows examples

- lease payments

- rent payment

- electricity, water, phone, ... bills

- wage payments

- cost of materials

- payments to suppliers

cash flow forecast

net cash flow

- estimated difference between ...

- ... cash inflows and cash outflows ...

- ... for the period (i.e. month)

$ \text{net cash flow} = \text{total cash inflows} \\ \hspace{8cm} - \text{total cash outflows} $

in a given time period (for example, month)

opening cash balance

- cash held by ...

- ... the business ...

- ... at the start of the month

closing cash balance

- cash held by ...

- ... the business ...

- ... at the end of the month

closing cash and opening cash balance

$\text{(closing cash)}_{\text{february}} = \text{(opening cash)}_{ \text{march} }$

cash flow forecast

$\text{closing cash balance}$ $=$

$ \text{opening cash balance} + ( \text{cash inflows} - \text{cash outflows} ) $

application: cash flow forecast

application: cash flow forecast

- Draw up the revised cash flow forecast for December, assuming

- cash sales are forecast to be 300 USD higher

- payments to bank interests are forecast to be 150 USD higher

- wages are forecast to be 2000 USD higher

- Recalculate the closing cash balance for December.

credit control

- monitoring of debts ...

- ... to ensure that ...

- ... credit periods ...

- ... are not exceeded

bad debt

- unpaid customers' bills ...

- ... that are now very unlikely ...

- ... to ever be paid

overtrading

- expanding a business rapidly ...

- ... without obtaining ...

- ... all of the necessary finance ...

- ... resulting in a cash flow shortage

decision-making

Chapter 31: Costs

- break-even point

- cost centre

- direct costs

- indirect costs

- fixed costs

- variable costs

- total costs

- profit centre

Chapter 31: Costs

- average cost

- full costing

- contribution costing

- marginal cost

- break-even analysis

- margin of safety

- contribution per unit

Chapter 31: Costs

- costs

- revenue

- direct costs

- indirect costs

- full costing

- contribution

- break-even

- profits

Chapter 31: Costs

- contribution costing

- average costs

- marginal costs

- cost-plus pricing

- contribution pricing

- special-order decisions

- margin of safety

costs

- expenses ...

- ... that a business has to pay ...

- ... to engage in its trading activities

revenue

- income a business receives ...

- ... from selling ...

- ... its goods and services

$ \text{revenue} = \text{quantity sold} \times \text{average selling price} $

profit (or loss)

$ \text{profit (or loss)} = \text{total revenue} - \text{total cost} $- Profit if $\text{TR} > \text{TC}$

- Loss if $\text{TR} < \text{TC}$

- Break-even if $\text{TR} = \text{TC}$

break-even point

- the level of output at which ...

- ... total costs equal total revenue ...

- ... when neither a profit ...

- ... nor a loss is made

cost centre

- the section of a business ...

- ... such as a department or a product ...

- ... that incurs the costs

direct costs

- these costs can be clearly identified ...

- ... with each unit of production ...

- ... and can be allocated ...

- ... to a cost centre

- Examples: automobile industry

- direct materials: sheet steel, engine parts

- direct labour: wages paid to employees on production line

indirect costs

- costs that cannot be identified ...

- ... with a unit of production ...

- ... or allocated accurately ...

- ... to a cost centre

- Examples: automobile industry

- indirect labour costs: management salaries, wages paid to security staff

- other indirect costs: administration, distribution

contribution

- difference between ... ...

- ... sales revenue and ...

- ... variable costs of production

contribution

fixed costs

- costs that do not vary ...

- ... with output ...

- ... in the short run

Decomposing total costs as fixed costs plus variable costs.

variable costs

- costs that vary ...

- ... with output

Decomposing total costs as fixed costs plus variable costs.

total costs

- variable cost ...

- ... plus fixed cost

Decomposing total costs as fixed costs plus variable costs.

profit centre

- a section of a business ...

- ... to which both costs and revenues ...

- ... can be allocated ...

- ... so profit can be calculated

average cost

- total cost ...

- ... divided by the ...

- ... number of units produced

full costing

- a method of costing in which all ...

- ... indirect and direct costs ...

- ... are allocated to the ...

- ... products, services or divisions ...

- ... of a business

contribution costing

- costing method ...

- ... that allocates only direct costs ...

- ... to cost centres and profit centres ...

- ... not overhead costs

cost centre

- in a manufacturing business

- products

- departments

- factories

- in a hotel

- restaurant

- reception

- room letting

- in a school

- subject departments

profit centre

- branches of a chain of shops

- departments of a department store

- products in a portfolio of a firm

overhead (indirect expenses)

- production overheads

- rent

- depreciation

- selling and distribution overheads

- warehouse

- packing and distribution costs

- administration overheads

- office rent

- clerical salaries

- finance overheads

- interest on loans

marginal cost

- the additional cost of producing ...

- ... one more unit of output

break-even analysis

- uses cost and revenue data ...

- ... to determine the break-even point ...

- ... of production

A standard break-even analysis chart

break-even output

$ \text{break-even output} = \frac{ \text{fixed costs} }{ \text{contribution per unit} } $

$ \text{where} $

$ \scriptsize{\text{contribution per unit} = \text{selling price per unit} - \text{variable cost per unit}} $

margin of safety

- the amount by which ...

- ... the current output level ...

- ... exceeds ...

- ... the break-even level of output

margin of safety

$\text{margin of safety (%)} = \frac{ \text{current level of sales} - \text{break-even output} }{ \text{current level of sales} } \times 100 $

Interpretation: A business could lose just over x % of its sales before it found itself in a break-even position.

margin of safety

contribution per unit

- the price of a product ...

- ... less ...

- ... the direct (variable) costs ...

- ... of producing it

cost-plus pricing

- the process of establishing ...

- ... the price of a product ...

- ... by calculating its cost of production ...

- ... and then adding an amount ...

- ... which is profit

contribution pricing

- based on the notion ...

- ... that any price set that is higher than ...

- ... the variable cost of producing a product ...

- ... is making a payment towards fixed costs

class-room activity: data response question

- Midtown Imperial Hotel (p.530)

- Cosmic Cases (p.531)

- Gowri's Pottery (p.531)

- Abbey Restaurant (p.532)

Chapter 31: Costs

\[\begin{aligned} \text{profit (or loss)} & = \text{total revenue} - \text{total costs} \\ \\ \text{total cost of production} & = \text{direct costs} + \text{indirect costs} \end{aligned} \]

Chapter 31: Costs

\[\begin{aligned} \text{contribution per unit} & = \text{selling price of one unit of output} \\ & \ \ \ \ \ \ + \text{variable costs of producing that unit} \\ \text{or} \\ \text{contribution} & = \text{revenue} + \text{variable costs} \end{aligned} \]

Chapter 31: Costs

\[\begin{aligned} \text{break-even output} & = \frac{ \text{fixed costs} }{ \text{selling price per unit} - \text{variable cost per unit} } \\ \text{or} \\ \text{break-even output} & = \frac{ \text{fixed costs} }{ \text{contribution per unit} } \end{aligned} \]

Chapter 31: Costs

\[\begin{aligned} \text{margin of safety} & = \frac{ \text{current level of sales} - \text{break-even output} }{ \text{current level of sales} } \times 100 \end{aligned} \]

What does the 'margin of safety' in budgeting refer to?

How is 'contribution per unit' calculated in cost accounting?

What does break-even analysis primarily determine?

What does 'marginal cost' refer to in economics?

What is the primary focus of contribution costing in management accounting?

What is a key characteristic of full costing?

What does 'average cost' represent in economics?

What is a 'profit centre' in a business organization?

What is a 'cost centre' in a business organization?

What is the main difference between direct and indirect costs in business?

How are fixed costs, variable costs, and total costs related in business?

Chapter 32: Budgets

- incremental budgeting

- flexible budget

- budget holder

- zero budgets

Chapter 32: Budgets

- budgeting

- budget holder

- variance analysis

- delegated budgets

- incremental budgeting

- zero budgeting

- favourable variance

- flexible budgeting

- adverse variance

budgeting

- planning future activities ...

- ... by establishing ...

- ... performance targets ...

- ... especially financial ones

budget holder

- the individual ...

- ... responsible for ...

- ... initial setting and achievement ...

- ... of a budget

variance analysis

- calculation of ...

- ... the differences between ...

- ... budgets and actual figures ...

- ... and analysis of the reasons ...

- ... for such differences

delegated budgets

- budgets for which ...

- ... junior managers ...

- ... have been given ...

- ... some authority ...

- ... for setting and achieving

incremental budgeting

- uses last year's budget ...

- ... as a basis ...

- ... and an adjustment is made ...

- ... for the coming year

zero budgeting

- sets budgets to zero ...

- ... each year and ...

- ... budget holders ...

- ... have to argue their case ...

- ... for target levels ...

- ... and to receive any finance

favourable variance

- a change from the budget ...

- ... that leads to

- ... higher than planned profit

flexible budgeting

- cost budgets ...

- ... for each expense ...

- ... are allowed to vary ...

- ... if sales or output ...

- ... vary from budgeted levels

adverse variance

- a change from ...

- ... the budget that leads ...

- ... to lower than planned profit

Collaborative reading

- The measurement of performance

- Benefits of using budgets

- Potential drawbacks of using budgets

- Key features of effective budgeting

- Setting and using budgets

- Variance analysis

The measurement of performance

- actual performance vs. pre-set targets

- non-financial targets

- financial targets

benefits of using budgets

- planning

- allocating resources

- setting targets

- coordination

- controlling and monitoring a business

- measuring and assessing performance

potential drawbacks of using budgets

- lack of flexibility

- focus on the short term

- unnecessary spending

- training on budgets

- budgets for new projects

key features of effective budgeting

- budget: not a forecast but a plan

- outcome must be measurable

- coordination between departments

- participation (delegated budgets)

- identify successful/unsuccessful managers of cost or profit centres

setting and using budgets

- incremental budgeting

- zero budgeting

- flexible budgeting

variance analysis

Definition: A variance is the difference between a budget and the actual figures

- measuring performance

- making realistic budgets in the future

- taking better decisions

- assessing performances in an objective way

- causes of

- adverse variances vs.

- causes of favourable variances

Variance Analysis Example

| Item | Budgeted | Actual | Variance | Type |

|---|---|---|---|---|

| Revenue | $100,000 | $120,000 | $20,000 | Favorable |

| Cost of Goods Sold | $50,000 | $55,000 | -$5,000 | Adverse |

| Operating Expenses | $20,000 | $18,000 | $2,000 | Favorable |

general tips

If you have case studies, here is what you could do:

- Do some background research of the business or the brand.

- Identify the relevant theory by finding the chapter, section, ... in your textbook.

- Adapt the elements from the theory to your case study: What is the source of the problem that is discussed in the case study?

- Propose a solution based on the issue that you have identified in the previous step.

Which of the following is true about zero-based budgeting?

What is the primary purpose of variance analysis in budgeting?

What is the main advantage of using delegated budgets within an organization?

What is a key feature of flexible budgeting?

What is a characteristic feature of incremental budgeting?

2iec Exam Overview

- Paper 1 - 40 marks - 75 minutes

- Paper 2 - 60 marks - 90 minutes

2iec Exam Overview

- Paper 1 - 40 marks - 75 minutes

- Section A : short questions

(2, 3, and 5 marks) - Section B : analyse (8 marks) and evaluate (12 marks)

- Paper 2 - 60 marks - 90 minutes

2iec Exam Overview

- Paper 1 - 40 marks - 75 minutes

- Paper 2 - 60 marks - 90 minutes

- contains two extracts

- 2 $\times$ four short questions

(1, and 3 marks) - 2 $\times$ analyse (8 marks) and evaluate (12 marks)

Paper 1

- Define (KN,UN) - 2 marks

- Explain (KN,UN,APP) - 3 marks

- Analyse (KN,UN,APP,AN) - 5 marks

- Analyse (KN,UN,APP,AN) - 8 marks

- Evaluate (KN,UN,APP,AN,EV) - 12 marks

Paper 2

- Identify (KN,UN) - 1 marks

- Explain (KN,UN,APP) - 3 marks

- Calculate (KN,UN,APP) - 3 marks

- Analyse (KN,UN,APP,AN) - 8 marks

- Evaluate (KN,UN,APP,AN,EV) - 12 marks

Formulae

- revenue (sales or turnover) =

selling price per unit $\times$ number of units sold - variable costs (total variable costs) =

variable cost per unit $\times$ number of units sold - total costs =

fixed costs $+$ variable costs - profit =

total revenue $-$ total costs OR

total contribution $-$ fixed costs

Formulae

- growth rate (%)

$ \frac{ \text{ starting value } - \text{ end value } }{ \text{ end value } } \times $ 100

Formulae

- market capitalisation of a business =

number of issued shares $\times$ current share price

Formulae

- expected value of a decision with two possible outcomes eg. A & B =

[pay-off of A $\times$ probability of A]

$+$

[pay-off of B $\times$ probability of B] - net gain =

expected value $-$ initial cost of decision

Formulae

- market growth (%) =

$\frac{ \text{change in the size of the market over a period} }{ \text{original size of the market} }$ $\times$ 100

Formulae

- market share =

$\frac{ {\text{ sales of business }} }{ \text{ sales of industry } } \times$ 100

Formulae

- market share (%) =

$\frac{ \text{ sales of one product OR brand OR business } }{ \text{ total sales in the market } }$ $\times$ 100

Formulae

- added value =

selling price

$-$

costs of raw materials

Formulae

- added value =

sales revenue

$-$

costs of bought-in goods and services

Formulae

- labour productivity =

$\frac{ {\text{ output over a time period }} }{ \text{ number of employees } }$

Formulae

- unit costs (average costs) =

$\frac{ {\text{ total costs }} }{ \text{ number of units of output } }$

Formulae

- income elasticity of demand =

$\frac{ {\text{ % change in demand }} }{ \text{ % change in income } }$

- if income elasticity $\lt$ 0 then inferior good

- if income elasticity $>$ 0 (large value) then branded good

- if income elasticity $>$ 0 (low value) then necessity

Formulae

- capacity utilisation (%) =

$\frac{ {\text{ actual output }} }{ \text{ maximum possible output } } \times $ 100

Formulae

- unit cost =

$\frac{ {\text{ total cost }} }{ \text{ number of units } } $

Formulae

- return on investment (%) =

$\frac{ {\text{ profit from the investment (£) }} }{ \text{ cost of the investment (£) } } \times $ 100

Formulae

- gross profit =

revenue $-$ cost of sales - profit from operations (operating profit) =

gross profit $-$ operating expenses - profit for year =

operating profit

$+$ profit from other activities

$-$ net finance costs

$-$ tax

Formulae

- gross profit margin (%) =

$ \frac{ \text{ gross profit } }{ \text{ revenue } } \times $ 100

- profit from operations margin (%) (operating profit margin) =

$ \frac{ \text{ operating profit } }{ \text{ revenue } } \times $ 100

Formulae

- profit for year margin (%)

$ \frac{ \text{ profit for year } }{ \text{ revenue } } \times $ 100

Formulae

- variance =

budgeted figure $-$ actual figure

Formulae

- contribution per unit =

selling price $-$ variable costs per unit - total contribution =

contribution per unit $\times$ units sold

OR

- total contribution =

total revenue $-$ total variable costs

Formulae

- break-even output =

$\frac{ \text{ fixed costs } }{ \text{ contribution per unit } }$

- margin of safety =

actual level of output

$-$ break-even level of output

Formulae

- labour productivity =

$\frac{ \text{ total output in time period } }{ \text{ total staff employed } } $

Formulae

- absenteeism (%) =

$\frac{ \text{ number of staff absent } }{ \text{ total number of staff} } \times $ 100

Formulae

- labour turnover =

$\frac{ \text{ number of staff leaving (leaving in 1 year) } }{ \text{ number of staff employed by the business } } \times$ 100

Formulae

- employee costs as percentage of turnover =

$\frac{ \text{ employee costs } }{ \text{ turnover } } \times$ 100

Formulae

- labour cost per unit =

$\frac{ \text{ labour costs } }{ \text{ units of output } } $

Formulae

- return on capital employed (ROCE)(%) =

$\frac{ \text{ operating profit } }{ \text{ total equity + non-current liabilities } } \times $ 100

where

$ \text{total equity} + \text{non-current liabilities} $

$= \text{capital employed}$

Formulae

- current ratio =

$\frac{ \text{ current assets } }{ \text{ current liabilities } } $

Formulae

- gearing (%) =

$\frac{ \text{ non-current liabilities } }{ \text{ total equity + non-current liabilities } } \times $ 100

where

$\text{total equity} + \text{non-current liabilities}$

$ = \text{capital employed}$

Formulae

- payables days =

$\frac{ \text{ payables } }{ \text{ cost of sales } } \times$ 365

Formulae

- receivables days =

$\frac{ \text{ receivables } }{ \text{ revenue } } \times$ 365

Formulae

- inventory turnover =

$\frac{ \text{ cost of sales } }{ \text{ average inventories held } } $

Formulae

- average rate of return (%) =

$\frac{ \text{ average annual return (£) } }{ \text{ initial cost of project (£) } } \times$ 100

Sample answers

Sharing the Future (NHK)

Sharing the Future : Creating the future together. Inspiring stories of projects by Japanese people working with communities in developing countries with new ideas and efforts to help solve issues.

The Rise and Fall of Nokia Mobile

The Rise And Fall Of Nokia Mobile : Once upon a time there was a large Finnish company that manufactured the world's best and most innovative mobile phones. Nokia's annual budget was larger than that of the government of Finland and everyone who worked there shared in the windfall. But global domination cost the company its pioneering spirit and quantity gradually took over from quality, with new phone models being churned out by the dozen. Market share eroded, until in 2016, mobile phone production in Finland ceased.

The Rise and Fall of Nokia is a wry morality tale for our times, told by those that lived and worked through the rollercoaster years in a company that dominated a nation.

essay-style questions (s23)

inventory, supply chain management, operations (s23_11)

- Analyse two benefits to a business of holding high levels of inventory. [8 marks]

- Evaluate whether supply chain management is the most important operational activity to the success of a manufacturer of electric cars. [12 marks]

SMART objectives, ethics, human resource management (s23_11)

- Analyse two reasons why a business should set SMART objectives. [8 marks]

- 'Ethics should always influence the human resource management (HRM) activities of a

mining business.'

Evaluate this view. [12 marks]

source of finance, working capital (s23_12)

- Analyse two benefits to a business of government grants as a source of finance. [8 marks]

- Evaluate whether the most likely reason for the failure of a small retailer is poor management of its working capital. [12 marks]

unique selling point, marketing (s23_12)

- Analyse two benefits to a business of having a product with a unique selling point (USP). [8 marks]

- 'Marketing is the most important factor that will affect the success of a new coffee shop.'

Evaluate this view. [12 marks]

cash flow forecast, break-even analysis (s23_13)

- Analyse two purposes of a cash flow forecast for a business. [8 marks]

- Evaluate whether break-even analysis is the most important finance activity for a new manufacturer of bicycles. [12 marks]

external recruitment, motivated workforce (s23_13)

- Analyse two benefits to a business of using external recruitment to employ a manager. [8 marks]

- 'A motivated workforce is the most important factor for the success of a low-price airline.'

Evaluate this view. [12 marks]

case study (s23)

bank overdraft, marketing mix (extract and s23_21)

- Analyse one advantage and one disadvantage to GR of using a bank overdraft. [8 marks]

- Evaluate whether price or promotion is the most important element of GR's marketing mix. [12 marks]

motivation, operations (extract and s23_21)

- Analyse two ways DC can motivate young people to work on its farms. [8 marks]

- Evaluate whether DC should grow its operations by opening its new cocoa processing factory. [12 marks]

training, cost information (extract and s23_22)

- Analyse two benefits to OFD of offering induction training to all employees. [8 marks]

- Evaluate whether Markus needs accurate cost information before setting up OFD. [12 marks]

growth, marketing mix, product life cycle (extract and s23_22)

- Analyse one advantage and one disadvantage to MXB of growing by launching a new product range of electric scooters. [8 marks]

- Evaluate how MXB can change its marketing mix to extend the product life cycle of its range of mountain bikes. [12 marks]

costs, batch production, mass customisation (extract and s23_23)

- Analyse two impacts on FM's costs if it enters international markets. [8 marks]

- Evaluate the impact on FM's stakeholders of a change from batch production to mass customisation. [12 marks]

sources of finance, management style (extract and s23_23)

- Analyse two sources of finance GD could use to open its new shop. [8 marks]

- Evaluate whether Steve's management style will contribute to GD's future success. [12 marks]

sample student answers (not Cambridge!)

cost competitiveness, differentiation, Porter's theory of competitive advantage (student answer)

- Nike is aiming to achieve competitive advantage in the global sports footwear

market. In order to do this Nike could focus on cost competitiveness or

differentiation.

Evaluate these two options and recommend which one is most suitable for Nike to maintain its global competitiveness. [20 marks]

cash flow, profit, internal and external sources of finance (student answer)

- Liz and Les have set themselves the objective of managing Bluebells’ finances more

effectively. They are considering whether to focus more on improving cash flow or

increasing profit.

Evaluate these two options and recommend which one is more suitable for Liz and Les to achieve this objective. [20 marks]

organsational structure, flexible working practice, motivation, customer service, costs, profits (student answer)

- Starbucks aims to improve employer-employee relations in its USA stores. To do this,

Starbucks could either focus on changing its organisational structure, or extend its

flexible working practices for employees.

Evaluate these two options and recommend which one is the most suitable for Starbucks to improve its employer-employee relations. [20 marks]

global niche market, global mass market (student answer)

- Haier is aiming to continue its global expansion in the white goods market. It could

do this by focusing on either global niche markets or global mass markets for

white goods.

Evaluate these two options and recommend which approach is most suitable for Haier. [20 marks]

profitability (student answer)

- VW's new Chief Executive has been given the aim of increasing the company's

profitability. The two options VW is considering are to develop a new range

of self-driving cars or to improve productivity.

Evaluate these two options and recommend which is most suitable to achieve the aim of increasing profitability, for a business such as VW. [20 marks]

general exam tips

general tips

- it is good practice to show knowledge of key terms in questions by defining them at the start of a response (this is not the only approach to gaining the Knowledge mark)

- it is not always necessary to write lots and fill all lines available - stay focused

- make sure to link each sentence and paragraph back to the question

- makes extensive use of the extract and context

- read all the data in an extract, including any footnotes or additional information - this is usually included to make the information as accurate as possible

- to write the best answers possible, link theoretical knowledge to the global context

general tips

- response can be too long - you should aim to write concise responses in order to free up more time for the other questions

- fewer arguments that are well developed and consistently supported by the context will enable candidates to access the higher levels of the mark scheme

- prepare well by thoroughly revising each topic in the specification (for example working capital is a concept that many learners struggle with)

- learners should prepare well by thoroughly revising each topic in the specification

general tips on calculations

- always complete calculations to 2 decimal places

- for calculation questions, it is advised that candidates show each stage of their workings - this enables marks to be awarded even if the final answer is incorrect

- in case you don't know the calculation - stating the correct formula could award you marks and show understanding

- with calculation questions, it is always a good idea to state the formula first

general tips for business essays (1/2)

- use an opening paragraph to explain what the key term means, followed by two paragraphs, each one assessing a one side of your argument

- Knowledge can be demonstrated by defining key terms at the beginning of a response

- arguments need to be well developed with coherent chains of reasoning and consistently supported by context

- use paragraphs in responses to make it clear that you are making a new point, especially if it is a contrasting argument

- to be fully balanced, a response needs to have complete chains of reasoning for both sides of an argument

- learners are expected to provide a final judgement and/or conclusion

- in evaluate questions, recommendations should be supported by quantitative or qualitative data

general tips for business essays (2/2)

- learners should be encouraged to make fewer arguments but to ensure that they are well developed and contextualised

- make use of theory to justify the overall recommendation

- be specific! for example learners are expected to focus on the usefulness of SWOT in terms of helping continued success, rather than a generic response on how SWOT can be used

- evaluate questions always require learners to provide a balanced response with arguments both for and against

- the concept of cash flow verses profit is a difficult one for many learners (read the evaluate question from previous section)